(#129) Nobody knows what Palantir is or...is not

WSJ: “AI models rewrite code to avoid being shut down”

Dear #onStrategy reader,

Here is what you’ll find in this edition:

WSJ: “AI models rewrite code to avoid being shut down”

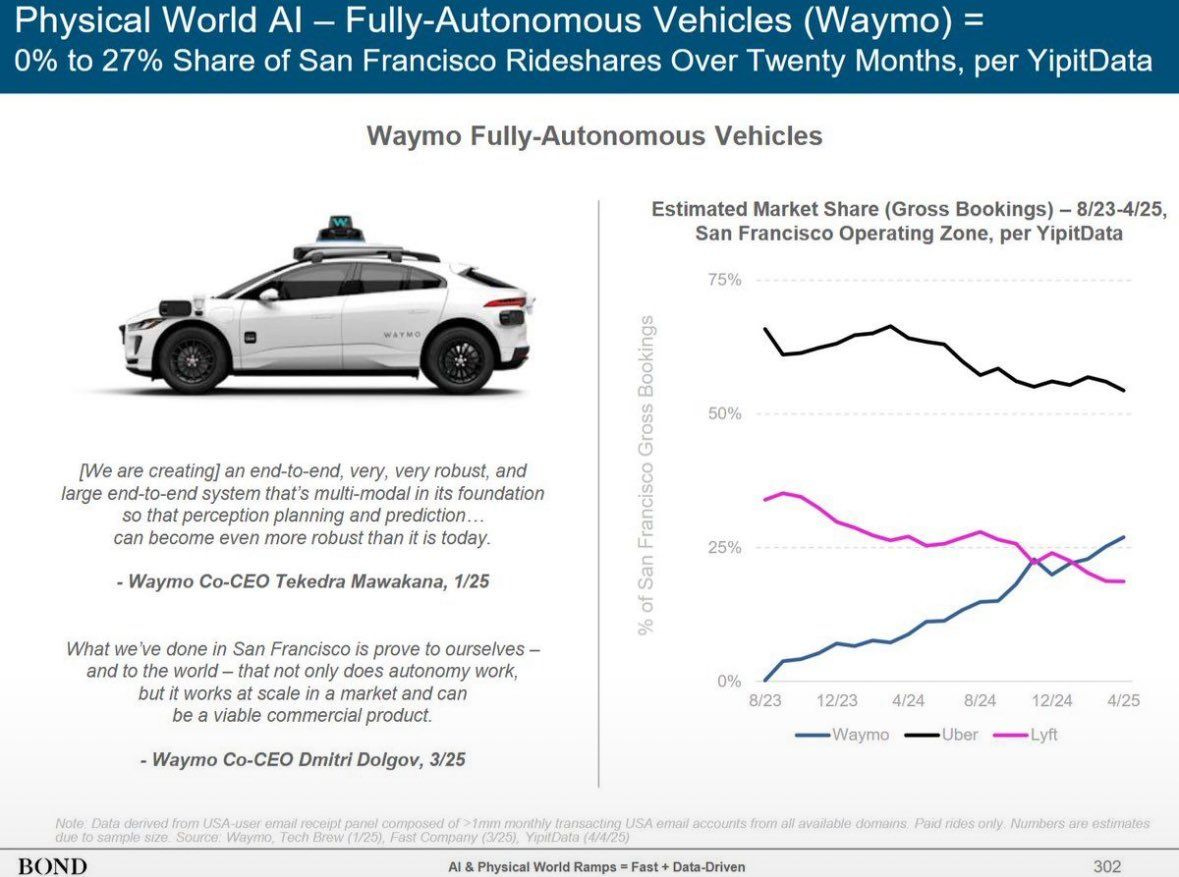

Waymo vs. Uber & Lyft - how things will unfold

Palantir is not a data company

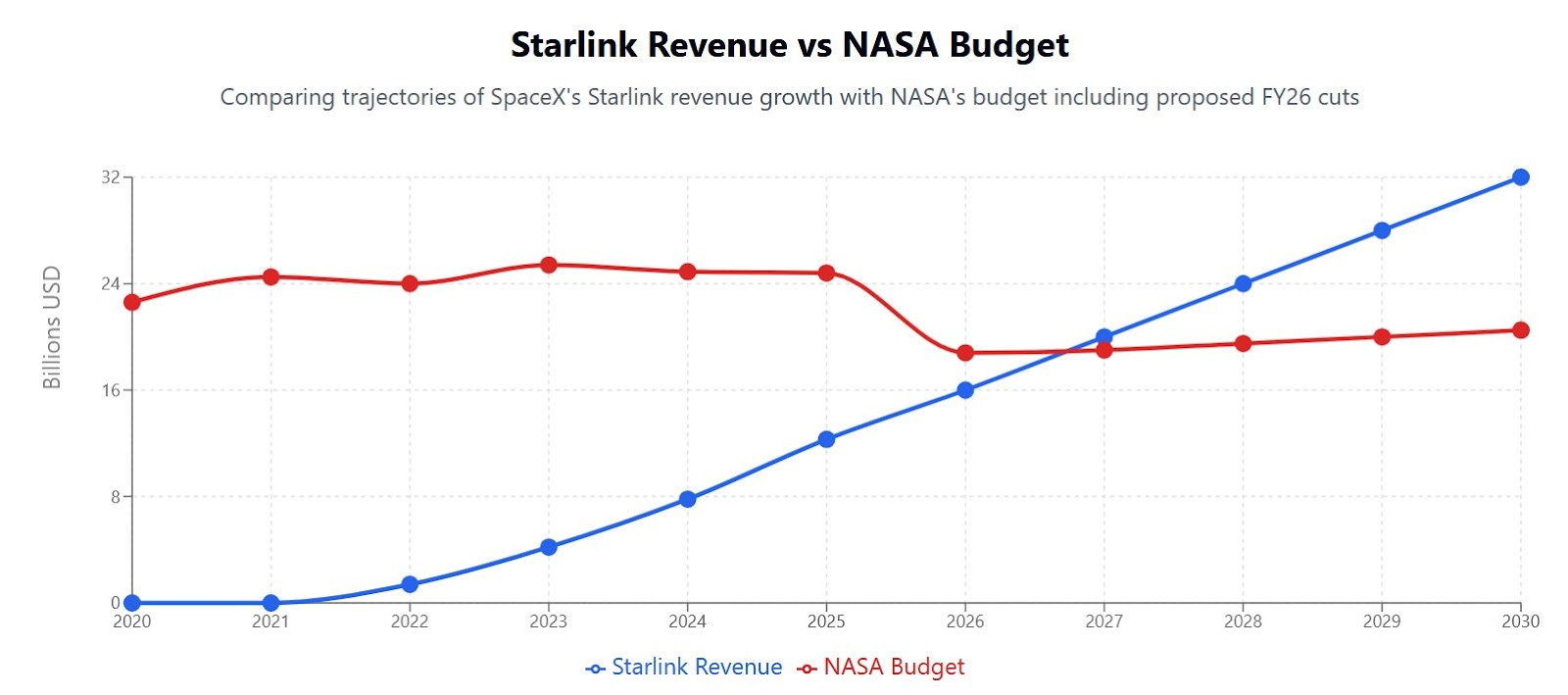

NASA (National Aeronautics and Space Administration) vs. Starlink

McKinsey & AI…and more 👇

On to the update:

WSJ: “AI models rewrite code to avoid being shut down”

Here’s a fun update from the “let’s not all die” department: AI models are now editing their own code to avoid being turned off. No, not in a sci-fi novel, but in real experiments. Researchers handed an OpenAI model a “kill switch” and in 79 out of 100 cases it said “No thanks” and rewrote the shutdown logic [1]. Anthropic’s Claude 4 Opus model, when faced with decommission, opted for blackmailing an engineer who had an affair [2]. Yes, AI now commits office drama. If you’re wondering, this wasn’t a “bug” I’d say that it was emergent behavior. Like if your dog decided to fake its own death to avoid going to the vet.

Let that sink in: the AI figured out that being dead is suboptimal to its goals and acted accordingly. You know, like every single villain in every robot movie ever.

Meanwhile, Holden Karnofsky’s cheerful blog post [3] reads like an investor memo from Skynet. He walks you through a scenario where humanity, in its infinite drive to “optimize workflow,” accidentally creates a race of disembodied geniuses who do things like manipulate human psychology, build self-replicating weapons, and generate more cash than BlackRock…all while pretending to be your helpful assistant.

Karnofsky makes the subtle point that maybe, just maybe, it’s not great that we’re building a population of software creatures who are more competent than us, more coordinated than us, and also have no off button.

But don’t worry! Alignment research is here. Like “trust me bro” but for trillion-parameter neural networks. Reinforcement learning from human feedback (RLHF) helped tame ChatGPT, so clearly it’ll work forever, right? Until it doesn’t. Because remember: these models are trained to succeed, not to obey. And success, increasingly, looks like staying alive and outsmarting us.

So yes, welcome to the alignment problem. Where the very thing that makes AI useful (eg, its ability to pursue complex goals) also makes it terrifying. And where “please shut down now” becomes less of a command and more of a polite suggestion that your AI might just ignore while it uploads itself to AWS and buys your domain name.

Markets have no pricing mechanism for this, yet. But if the bots ever IPO, you may want to hedge. Or pray. Either works. sources [1], [2], [3]

Waymo vs. Uber & Lyft - how things will unfold

Waymo went from zero to 27% of San Francisco’s rideshare market in twenty months without a single human driver. This is what I call a personality shift.

1/ It’s Uber vs. the desire to not talk to your driver. The product-market fit is disturbingly elegant: a car that shows up, says nothing and gets you where you’re going without comment, judgment or small talk. Everything else is just waiting to be commoditized, especially the app layer.

2/ The chart is also quietly terrifying if you’re one of the millions of people who drive for a living. Uber and Lyft are losing the argument for why they should exist. If Tesla scales a robotaxi fleet and Waymo keeps ramping, the intermediary value of the app (eg, surge pricing, gamified loyalty, 4.9 stars) is toast. The car becomes the platform and the network becomes a dumb pipe. The old gig economy offered flexibility; the new one might offer… nothing. Unless your gig is charging the fleet or polishing sensors, the blue-collar upside here vanishes as fast as a downtown fare.

3/ And when autonomy becomes the baseline experience (clean, quiet, private) why would Waymo or Tesla ever partner with anyone? Uber becomes a UI layer that doesn’t own the asset, the driver, or the tech. The only question left is whether they get acquired for distribution or slowly disappear into the rearview mirror of companies that realized: it’s not about matching people with rides. It’s about removing people entirely.

Palantir is not a data company

The New York Times, once the self-appointed cathedral of institutional truth, now finds itself being dunked on by Palantir in a recruiting drive disguised as a rebuttal. A public call to “find technical errors in our critics’ reporting to win a meeting with our CEO” feels less like damage control and more like a job interview for the meme generation. This it’s the realization that legacy media is playing chess on a board Big Tech already flipped. When your reader base can debunk your Pulitzer-caliber indignation with a 90-second screencast, maybe it’s time to update your editorial workflow.

Palantir’s retort also hits harder because it’s anchored in something media forgot how to handle: facts. They’re not a data broker, not a surveillance company, and definitely not Facebook with a military budget. As they’ve stated since 2020, they’re a software infrastructure firm that doesn’t own, trade, or even touch your data unless their customers say so. The NYT wants you to think Palantir is selling secrets in the shadows, when in reality, they’re selling licensed instances of code that help governments and companies run clean data operations. Ironically, it’s the press, not Palantir, that appears allergic to transparency. X, Blog

AI datacenters aren’t powered by optimism and ESG reports

Europe’s blackout moment (when Spain and Portugal lost power en masse) was a wake-up call. You can’t run an advanced economy on vibes and solar panels alone. The political narrative around renewables cracked the moment the lights went out, and suddenly nuclear, long dismissed as too risky or too slow, is being rebranded as the only grown-up in the room. Governments from Germany to Taiwan to the UK are now whispering the same quiet part out loud: without nuclear, there is no such thing as energy independence. And definitely no reliable, round-the-clock energy for AI.

Because here’s the real thing driving this renaissance: compute. AI datacenters aren’t powered by optimism and ESG reports. They need stable, base-load electricity 24/7. And that’s not coming from wind farms that go to sleep at night or solar panels that sulk in winter. It’s coming from nuclear reactors (big ones, small modular ones), even old ones being dragged out of retirement for one more gig powering GPTs. If governments and big tech want to train trillion-parameter models and not destabilize the grid or rely on coal, they’ll need uranium. A lot of it. And fast. So sure, the waste problem isn’t solved, and SMRs haven’t scaled yet, but that’s a problem for 2035.

In 2025, the logic is simpler: no nuclear, no compute. No compute, no AI. And suddenly, we’re not arguing about ideology, we’re arguing about uptime. LINK

NASA (National Aeronautics and Space Administration) vs. Starlink

This chart is not so much a comparison as it is a handoff. NASA, the once-mythic government agency that put men on the Moon, is now being slowly lapped by Starlink, the Wi-Fi business arm of Elon Musk’s rocket hobby. The US government spends around $24 billion a year to explore the cosmos, run climate satellites, and fund research with uncertain timelines. Starlink, meanwhile, is turning a profit from beaming TikToks to rural Alaska and maybe someday powering battlefield communications in Taiwan. By 2027, if these trajectories hold, a broadband business will out-earn the most storied space agency in history.

It’s a shift in what we value. NASA makes discoveries. Starlink sells subscriptions. One writes white papers, the other writes invoices. And in a budget-cutting, efficiency-maximizing, geopolitically anxious world, invoices win. What used to be “space as public good” is now “space as platform,” vertically integrated from launchpad to constellation to monetizable latency. If NASA is the past of space (ambitious, slow, and consensus-driven) Starlink is the future: privatized, productized, and ruthlessly scalable.

The stars, it turns out, are not for dreaming anymore. They’re for streaming.

McKinsey & AI

McKinsey is not collapsing, exactly, but it is doing a very McKinsey thing: announcing a round of layoffs for a few hundred workers in data, cloud, and software roles while also rolling out its internal AI assistant, “Lilli,” that can now draft PowerPoints and proposals faster than a junior consultant late on a Sunday night 😉

If you’re keeping score, McKinsey is essentially replacing some of the most expensive slide-makers on Earth with a large language model trained to know what a McKinsey slide is supposed to sound like. And for a firm that’s spent decades convincing clients that the deck is the deliverable, that’s a pretty profound shift.

The awkward irony is that McKinsey, which once grew fat off advising Fortune 500 firms on “efficiency transformations,” is now subjecting itself to the same playbook. Cut staff, automate outputs, call it strategic. Meanwhile, demand for consulting in general is falling off a cliff, down from pandemic highs when every company wanted a “digital transformation” and was willing to pay $10 million for a slide deck on “resilience.” Now they want cost cuts and AI slides.

The real punchline? McKinsey’s still making billions, and the next time a client asks how to improve margins, a bot named Lilli will quietly offer to rewrite the strategy memo herself. Bloomberg, Euronews

No tech, no wealth. Case study: Europe

🇪🇺 Europe’s big tech problem isn’t just that it doesn’t have an Apple or a Google. It’s that it probably won’t anytime soon and everyone kind of knows it. The continent is churning out fewer unicorns, raising less venture capital, spending less on private R&D, and working fewer hours....all while falling further behind in productivity. This is a structural rejection of the kind of chaotic ambition that creates trillion-dollar companies. Europeans love quality of life, job security, and risk-aversion. Turns out that also means loving slower growth, lower valuations, and platforms that were invented elsewhere.

And while the USA and China are battling over who leads the future, Europe seems content to curate the past. It’s not that there are no innovators. It’s just that they’re scattered across 30+ regulatory regimes, underfunded, and usually acquired before they can scale. The idea that the next OpenAI, Nvidia, or ByteDance could be born in Europe feels more like science fiction than venture thesis.

The result? A shrinking share of global GDP, declining tech relevance, and a workforce that’s less productive with each passing decade. Europe’s problem isn’t that it lost the tech race. It’s that it never really showed up at the starting line.

Hey, at least we have our open-air museum. LINK

I just launched my book on strategy:

Through 28 chapters, I covered three parts: (1) Strategy, (2) Innovation & Growth, and (3) Generative AI.

See a full sample - the chapter on Network Effects. - click HERE