(#166) 💻 AI turns software into labor; 🚗 Why Europe doesn't have a Tesla

🤖 on Optimus and other physical robots

[Personal Promo]

I consider “Where is my MOAT?“ to be like a mini-MBA 😎

This week, my subscribers four five posts, five different lenses on the world.

Here’s the schedule for this week

26.02.2026 - Update on my portfolios - only for Premium (paying) subscribers

What changed, what didn’t, what I trimmed, what I added, and (most important) why.27.02.2026 - On memory chips

28.02.2026 - Updates on Spotify

01.03.2026 - Shopify company analysis

…and here is the schedule for the next week:

4 March - [Essay] Enterprise AI agents move into core workflows

5 March - Updates on NVIDIA, Novo Nordisk and Mercado Libre

6 March - Updates on Apple & Berkshire Hathaway

7 March - [Deep dive] Palantir

8 March - [Deep dive] Salesforce

If you find WIMM useful, please share it with a friend or a colleague. WIMM is free for one month ... plenty of time to decide if it’s worth keeping in your stack.

Dear OnStrategy Reader,

Here is what you will find in this issue:

[Long take] AI turns software into labor

🤖 on Optimus and other physical robots

Rich countries have ‘rich countries’ problems

Peak human capital?

The death of “just the news”?

When the cost of failure is too high, disruption becomes irrational

…and much more

Onto the update:

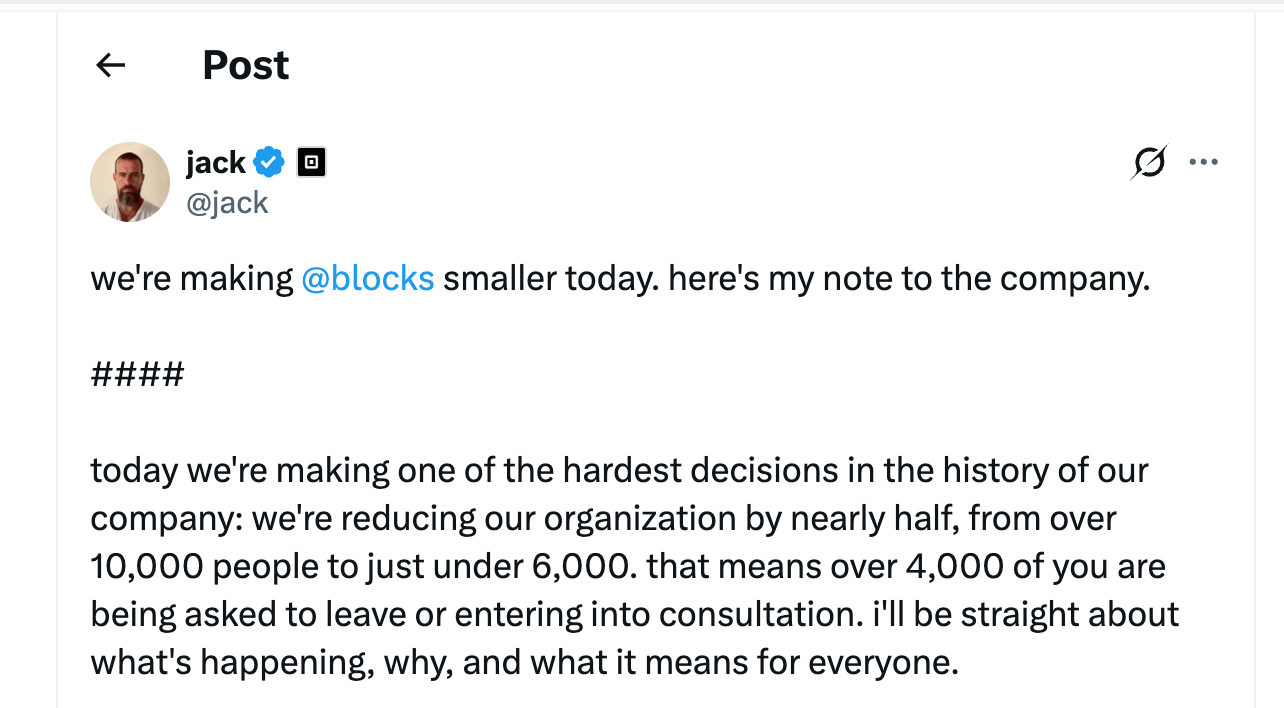

If AI turns software into labor, layoffs become pricing, and platforms win by becoming machine-readable.

Dorsey’s memo is doing two things at once:

(1) a classic “we’re getting smaller and flatter” restructuring; and

(2) a business model pre-announcement disguised as an org chart change.

The key line is the claim that “intelligence tools…paired with smaller and flatter teams…fundamentally changes what it means to build and run a company”. This is about admitting that the firm’s cost structure (and therefore its strategy) is being re-written by software that behaves like labor.

I already wrote in my “Where is my MOAT” article, “Is AI just the death of software?” about this next chapter for many companies. This is the “per-user to per-result” shift showing up inside the company before it shows up in the product. I argued that AI compresses the work that used to justify fat software margins (implementation, customization, workflow glue) and that the durable move is to stop selling seats, start selling outcomes, because agents do the work and the “user” becomes a supervisor. That logic doesn’t just pressure SaaS pricing, but also pressures its payroll. If you believe the unit of production is moving from “person-hours” to “agent throughput”, then “nearly half” is a forecast.

Now zoom into the last paragraph where Dorsey tells the remaining team they’ll help customers “build their own features directly, composed of our capabilities and served through our interfaces”. That is a platform strategy wearing a hoodie. Blocks’ wedge is “we expose primitives (payments, identity, risk, compliance, rails), then let customers assemble outcomes.”

Agents become a distribution and business model change. The buyer no longer wants a dashboard, but just a job done, and the easiest way to deliver that is to make your product legible to machines (APIs, workflows, composable modules) and let the customer’s agents orchestrate it.

The uncomfortable implication is that layoffs are the new “pricing page update”. If the market is repricing software because scarcity moved from UI to intelligence, then companies will reprice labor the same way with fewer people, higher leverage, more machine-readable surfaces. Most firms will try to compromise what I called out “cut costs and innovate,” i.e., “do the easy part aggressively and the hard part politely”.

Dorsey is betting on the opposite: do the hard part (org + product + interface strategy) in one traumatic move, so the company can actually rebuild around agents instead of defending a structure designed for seat-based work. Jack Dorsey, WIMM analysis

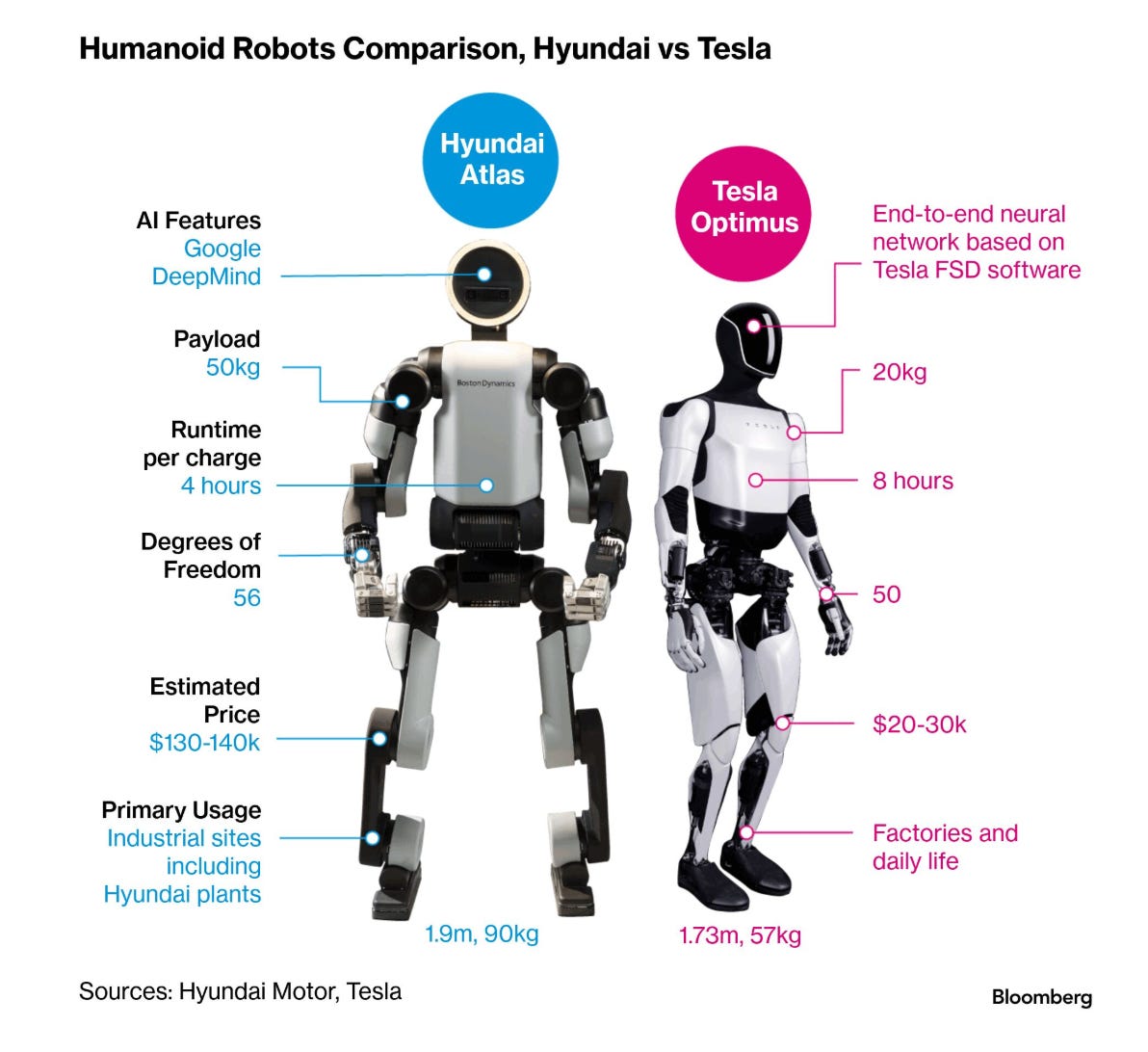

🤖 on Optimus and other physical robots

The interesting thing about Atlas vs. Optimus is that humanoids are the first credible attempt to turn AI from “software that talks” into “software that moves”. That’s a different kind of compounding. When AI sits behind a screen, its output is ideas, but when AI sits inside a body, its output is labor. Hyundai is explicitly aiming at high-volume repetitive tasks first (kitting components in 2028, more complex assembly by 2030), which is exactly how real automation wins, ie. narrow scope, measurable ROI, then expansion.

Strategically, this is also an “automakers as platforms” story, because a humanoid robot is basically an EV in disguise: batteries, motors, sensors, control systems, and increasingly, a software stack. That matters because car companies already know how to do the hardest part of robotics (ie. manufacturing at scale with acceptable defect rates). Hyundai buying Boston Dynamics and then pairing that hardware with AI partners (Nvidia, Google DeepMind) is the clearest sign that the car industry’s old advantage (factories) is being repurposed for the next advantage (factories that build workers).

The key tension is integration vs. components. Tesla’s pitch is end-to-end, where Optimus “inherits” Tesla’s FSD software approach and, if it really hits the $20-30k price range, it’s a mass-market wedge. Hyundai’s pitch is more like the classic industrial incumbent where Atlas is heavier-duty (50kg payload vs. 20kg) and aimed at industrial sites first, but it pays an “Nvidia tax” and relies on outside AI vendors, which can compress margins and slow iteration. In other words, Tesla wants to be Apple (integrated consumer scale), Hyundai looks more like a “best-of-breed” enterprise stack that wins by being deployable and useful now.

Zoom out and you get the real implication, where humanoids are a new labor supply curve. Bloomberg cites analyst math that at $100k, Atlas could work out to about $5/hour operating cost, below US federal minimum wage, and the whole investment case is "24/7 labor that doesn’t unionize, doesn’t quit, and gets software updates".

If that math holds even in a subset of tasks, it won’t just change factories; it changes bargaining power across manufacturing, warehousing, and eventually care work.

Concluding, the “AI race” is about distribution. Whoever has the real-world channels to deploy embodied AI at scale (factories, service networks, procurement relationships, safety certification muscle) gets to turn intelligence into cash flow before everyone else. Bloomberg

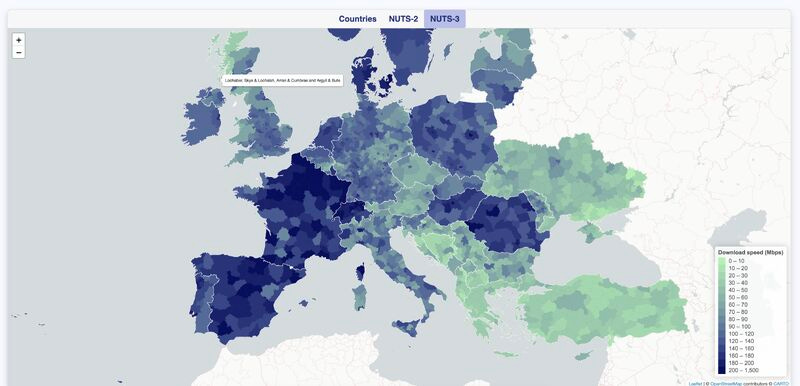

Get fast internet, or risk being an AI laggard economy

In 2026, “fast internet” is a social credential. If you don’t have serious bandwidth and low latency in the age of AI, nobody takes you seriously... not because they’re mean, but because your capability set is literally smaller.

You can’t reliably ship large models, run modern workflows, collaborate in real time, or even do the basic “I’ll just use the cloud” thing without turning every task into a loading-screen meditation.

You will then get this vicious loop where talent avoids you, firms don’t build there, remote work isn’t really remote, and “AI adoption” becomes a promise instead of an operating system.

Concluding, some regions are plugged into the future, and others are asking the future to please hold. LINK

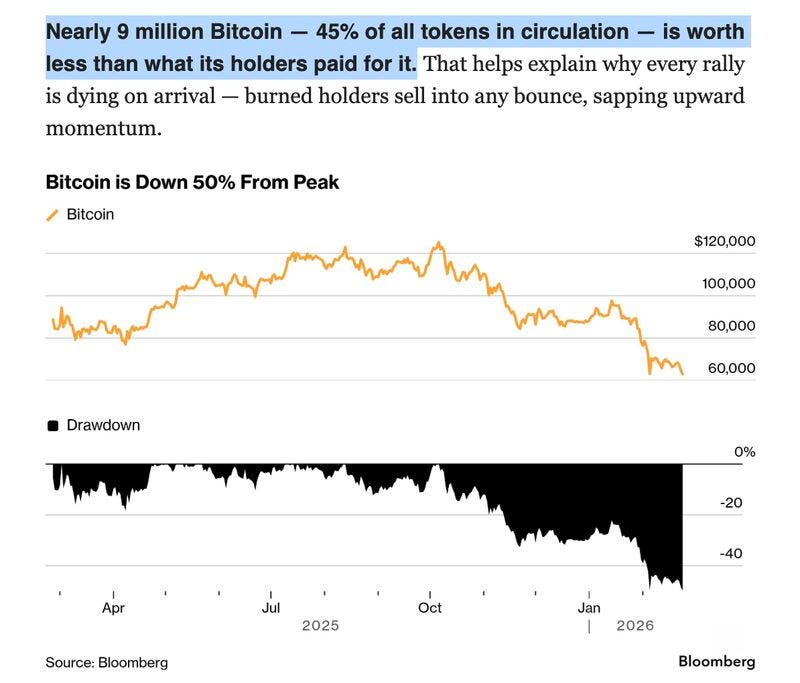

oh, Botcoin!

📈📉 This week on "Where Is My Moat?" I’m doing two things:

1/ a YTD look at my own portfolio (almost two months in)

and

2/ a deep dive on the current AI panic, including why the much-shared Citrini report has everyone spooked, and what the data actually says.

If you’re curious, you can try WIMM free for one month: ~20 articles in your inbox, plenty of time to see if it earns a permanent spot in your workflow.

🧐 Give it a shot and decide for yourself:

Rich countries have ‘rich countries’ problems

Bloomberg: "1 in 20 Australians use cocaine each year"

My two ideas on the topic:

1/ When a country gets rich, it tends to do drugs in the same way that when a company gets profitable, it tends to do stock buybacks. It’s not proof of virtue, it’s proof of capacity. You’ve solved (enough of) the “rice and rent” problems, you’ve built logistics, you’ve got disposable income, and, crucially, you’ve got a large class of high-functioning people who are exhausted, bored, ambitious, and trying to feel something on a Thursday night after a 14-hour day. “Developed market” is basically shorthand for “the demand curve has room for non-essentials” and cocaine is a non-essential with great unit economics.

2/ Australia is the cleanest case study because it has the audacity to be geographically inconvenient and still become, effectively, a premium-priced consumer market.

Wealth makes demand deep; remoteness makes supply expensive; expensive supply doesn’t kill the market, but it upgrades it. And then everyone acts shocked that organized crime is… organized. But the whole point of a high-margin product is that it finances unpleasant vertical integration: corruption, violence, recruitment of insiders, the whole bundle.

Rich countries don’t “fall into” drugs, but they create a market attractive enough that global supply chains (legal and illegal) re-route themselves to serve it.

Q.E.D.

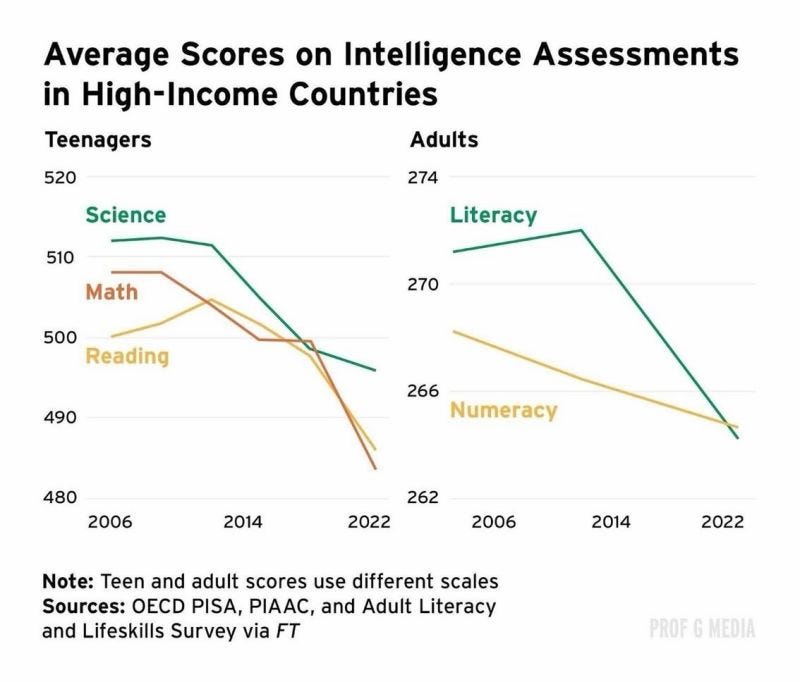

Peak human capital? (Reposting some ideas from two months ago, from Financial Times)

These charts are awkward. Teen science, math, and reading scores drift down after 2014, then fall harder into 2022. Adult literacy and numeracy bend the same way, with literacy taking a particularly sharp hit. You can blame pandemics, phones, curricula, … the government. Or you can zoom out and notice the timing.

The steepest declines arrive just as the smartphone became the default interface to the world and algorithmic feeds became the dominant cognitive environment. It is hard to prove causation, but it is also hard to ignore correlation when every spare moment is auctioned to short-form video.

The uncomfortable implication is not that AI makes us super dumb, but that we may be outsourcing first-order cognition long before AI fully arrives. If search reduced the need to remember, feeds reduce the need to focus, and generative tools may reduce the need to struggle. (Pls, read this paragraph again!)

The market rewards convenience, and convenience compounds. The question is whether societies can compound cognitive capital at the same time. If human intelligence scores are flattening while machine intelligence is accelerating, that gap becomes the most important spread trade of the next decade.

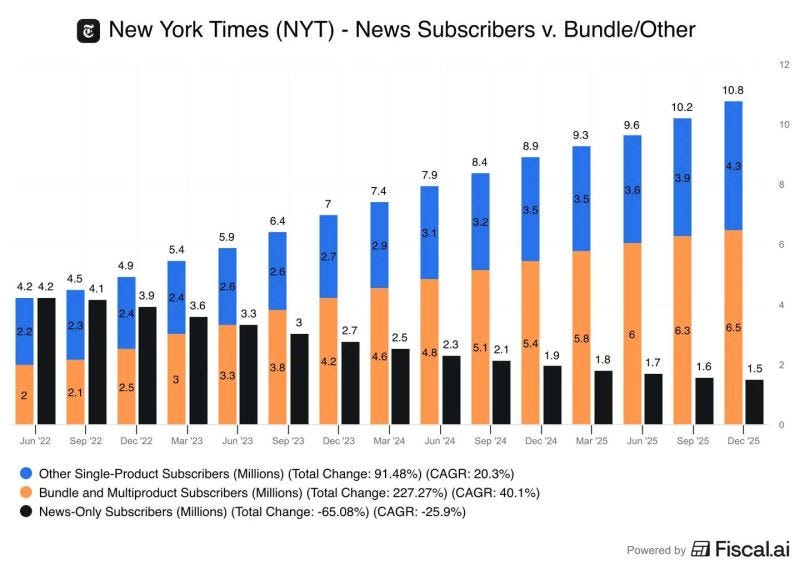

The death of “just the news”?

One way to read this chart is that The New York Times is no longer in the news business, but in the habit business 😅.

News-only subscribers are quietly melting away while bundle and multiproduct subscribers are compounding like a decent growth stock, which tells you that journalism by itself is a volatile product but journalism plus games plus cooking plus “something to do on your phone when you’re bored” is a subscription fortress.

The funny thing about bundling is that it looks like a discount but behaves like a moat. Once Wordle and recipes and product reviews are living in your daily routine, cancelling feels less like dropping a newspaper and more like uninstalling a lifestyle.

News may be cyclical and politically correlated and occasionally exhausting, but cross-subsidized attention is sticky. In other words, the Times figured out what Wall Street already knew, that diversification lowers risk, and apparently it also lowers churn.

When the cost of failure is too high, disruption becomes irrational

The core argument is straightforward but uncomfortable. Europe’s problem is not talent, capital, or even ambition... it is optionality. When the cost of failure is measured in 31 to 62 months of salary per employee in major economies, compared to seven in the United States, experimentation becomes structurally expensive. That changes corporate behavior at the margin, and at scale margins matter.

Radical innovation is a portfolio game: many shots, many misses, one or two massive hits. If shedding labor after a failed bet requires months of negotiation, regulatory approval, and nine-figure severance packages, the rational response is to avoid bets that might fail. Europe’s system is optimized for incremental improvement (note the steady decline in fuel consumption in combustion engines over decades) but poorly optimized for discontinuities like EVs or autonomy. Tesla is less a story about batteries than about the willingness to reallocate capital and labor quickly.

The more subtle point is that Europe’s model works... until the paradigm shifts. Long tenures, apprenticeship systems, and works councils build deep firm-specific knowledge; that is a feature in stable industries. It becomes a bug when software eats the drivetrain.

The irony is that startups are often exempt from these rules, but the exemptions disappear precisely when growth begins, which is when risk-taking needs to accelerate.

The countries that lean toward “flexicurity” demonstrate that the trade-off is not binary. You can protect incomes socially rather than protect jobs contractually.

In conclusion, Europe has optimized for sustaining innovation within existing value chains. The US has optimized for disruptive innovation that rewrites them. The result is not that Europe cannot build a Tesla. It is that its institutions make building, and especially failing while trying to build, one far more costly. LINK