(#167) 🏎️ Formula's One new strategy; ⏱️ on Rolex' strategy

A new management metric: “Elon speed”

I consider “Where is my MOAT?“ to be like a mini-MBA 😎

This week, my subscribers receive 5 posts. Here’s the schedule for this week:

4 March - [Essay] Enterprise AI agents move into core workflows

5 March - Updates on NVIDIA, Novo Nordisk and Mercado Libre

6 March - Updates on Apple & Berkshire Hathaway

7 March - [Deep dive] Palantir

8 March - [Deep dive] Salesforce

…and here is the schedule for the next week:

12 March - [Analysis] on the Middle East and some implications

13 March - [Essay] Workflow ownership is the next platform war.

14 March - [Deep dive] - Mastercard

15 March - [Deep dive] - Adobe

If you find WIMM useful, please share it with a friend or a colleague. WIMM is free for one month ... plenty of time to decide if it’s worth keeping in your stack.

Dear OnStrategy Reader,

Here is what you will find in this issue:

🏎️ Formula 1’s triple jump: New rules, new distributors, new entrants

A new management metric: “Elon speed”

Can you retire in China in a fake-Venice development with 1,200 RMB ($168) per month? Yes, you can!

New date from PISA tests. To think outside the box, you need to ‘put’ in the box

on Rolex’s & co strategy

on Shopify 🛍️

on Spotify 🎶

…and much more

Onto the update:

🏎️ Formula 1’s triple jump: New rules, new distributors, new entrants

Formula 1’s “pivotal year” is really a stress test of the Liberty Media playbook, which basically means, take a niche sport, wrap it in narrative (Drive to Survive), sell it as premium, then push distribution and sponsorship until it looks like a global consumer brand. The Financial Times piece shows the machine working with 2025 revenue up to $3.9bn and operating profit $632mn, with sell-outs (6.75m attendees) and a flood of sponsors that now includes everything from Doritos and Lego to luxury and AI brands. The twist is that F1 is now doing the hardest thing in media, which is, trading a known distribution partner (ESPN) for a deeper platform partnership with Apple, and betting that Apple can turn “watching races” into an integrated ecosystem moment across services (and even IMAX screenings), not just a TV slot. That’s classic “bundle leverage”, where Apple doesn’t need F1 to win sports, but it needs F1 to make Apple TV+ feel inevitable.

The second implication is the uncomfortable one. F1 is simultaneously upgrading its business model and rerolling its product. New 2026 regs mean smaller/lighter cars, a big shift toward electric power (50/50), and fully new builds (“not a bolt has carried over”), while some drivers complain it’s “anti-racing” and “less pure” because energy management rises in importance. This creates a mismatch risk where the new fanbase that arrived for characters and drama might tolerate technical changes, but the sport still needs the on-track spectacle to justify premium rights and premium sponsorship. Meanwhile, Cadillac and Audi add the “new entrants” halo, yet the article makes clear how brutally hard entry is (Cadillac hiring hundreds, drowning in applicants) and how much of the marketing upside depends on performance and possibly even a top-tier US driver, not just an American badge.

Put differently, 2026 is F1 attempting a rare triple jump: (a) platform distribution shift, (b) major product redesign, and c) expansion of the competitive set, while the flywheel is spinning. When it works, it compounds, but when it doesn’t, it breaks momentum. FT

A new management metric: "Elon speed"

The “world getting flatter” is really the world rediscovering a hard truth. When the core input is intelligence (and intelligence is increasingly software), coordination becomes the bottleneck. Hierarchies are coordination machines. They made sense when execution was scarce and information was expensive. In an AI-shaped firm, information is cheap, drafts are infinite, and the limiting factor is deciding what matters and shipping it. That’s why Meta building an “Applied AI Engineering” org with an ultra-flat ratio, up to 50 individual contributors per manager, is a more economic necessity.

Elon’s companies are the extreme expression of this with fewer layers, tighter loops, a single narrative, and a bias toward action that looks chaotic from the outside and efficient from the inside. The implication is that "flat" is a latency optimization. WSJ’s description of Meta’s new teams focusing on interfaces/tooling plus "executing tasks, generating data and providing evaluations" is basically a factory for the modern AI flywheel: ship → observe → evaluate → improve.

If you’re serious about model velocity, you can’t afford middle layers that turn feedback into meetings.

The second-order effect is strategic. As firms flatten, power shifts from managers to systems. Policies, evals, instrumentation, and internal platforms replace supervision. Your "manager" becomes the queue, the metric, the rubric, the deployment pipeline. That makes org design look more like product design. The best companies will be the ones with the cleanest internal APIs, the clearest incentives, and the strongest feedback loops ... because that’s what keeps a 50:1 org from becoming a 50:1 mess.

And the big implication for everyone else is that this convergence creates a new dividing line between companies that can operate at "Elon speed" and those that can’t. Flat structures reward high-agency talent and punish ambiguity. They also concentrate accountability and raise the cost of being wrong.

In the AI era, "flat" is a competitive weapon, but it’s also a stress test. If your culture can’t handle truth, speed, and ruthless prioritization, you’ll keep your org chart… and lose the decade. WSJ

on Meta’s “AI shopping research”

Meta’s “AI shopping research” tool is a land grab for the most valuable kind of search: the moment right before money moves. The strategic advantage is distribution + personalization. Meta already knows who you are, where you are, and what you like, and Bloomberg notes it tailors recommendations using signals like location and even gender inferred from a name. This is a shopping assistant that feels “for you”, inside the apps you already use.

The monetization question is the whole game. Does Meta take referral fees, and do advertisers get priority in the shortlist? Bloomberg flags both as open. If the answers become “yes”, Meta turns ads into “recommendations” and makes the auction about being chosen by the assistant, not just shown in a feed. The risk is trust. If users think it’s an ad unit in a chatbot costume, they bounce. We shall see. Bloomberg

Can you retire in China in a fake-Venice development with 1,200 RMB ($168) per month? Yes, you can!

This place exists because a debt-fueled property boom built 46,000 units for weekend fantasy buyers, then the boom broke, Evergrande went bankrupt, and occupancy fell to under 1 in 5. In other words, the same system that produced the grind (996 culture, hyper-competition, sky-high big-city costs) also produced the escape hatch, ie. an oversupply of homes priced like a utility bill.

The macro story is bigger than a few viral “lying flat” anecdotes. Beijing lost 1.6 million 20- and 30-somethings from 2019 to 2024, youth unemployment for 16-24 year-olds out of school sits around 16.5%, (official) growth runs at about 5% in 2025 (unofficial, is 1.5%), and suddenly the old bargain (ie. move to the megacity, climb the ladder) looks like a high-volatility trade with a drawdown you feel in your bones.

So young people are doing an elegant piece of balance-sheet management. They swap career upside for cost-of-living certainty, buy or rent apartments in places like Yunnan or Hegang where “apartments cheaper than cars” becomes a sales pitch, and finance “retirement” with savings plus modest online income streams.

This is both about a property bust and a generation deciding that time is the scarce resource. APNews

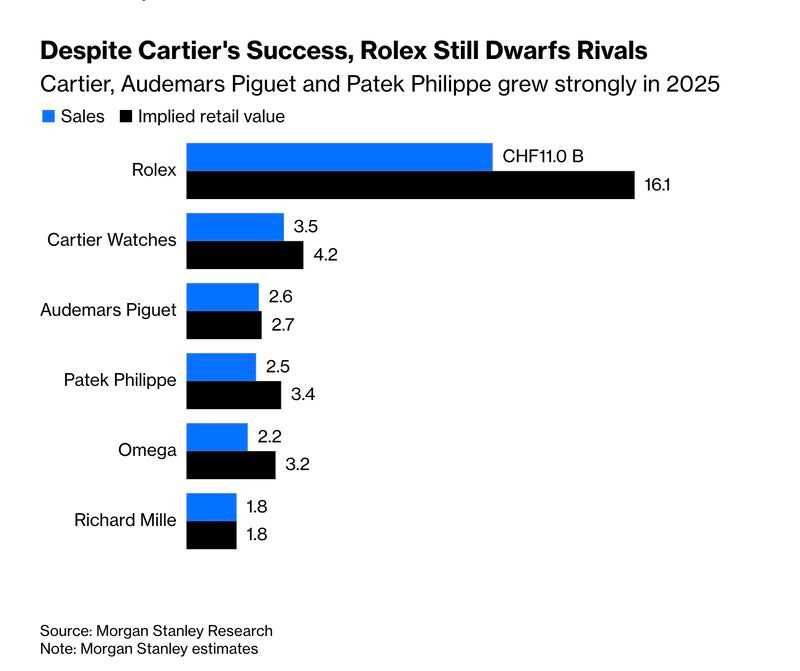

on Rolex’s & co strategy

For five years the luxury-watch business model was basically “negative inventory”. You walk into a store, they tell you nothing is available, and somehow that’s good news because it means the product is so desirable it has transcended commerce and become a social ranking system.

Now Bloomberg says "surprise, you might actually be able to walk out with a Rolex today".... maybe not the Rolex you want, but an actual Rolex with no sacred waitlist ritual. Of course this is being sold as a “turnaround” story, but it’s also just the hangover of the 2021-2023 era when people were flush with cash, stuck at home, and decided that buying an expensive mechanical object to mark time was a reasonable substitute for having plans.

Then in 2024-2025 the vibe shifted and experiences came back, costs went up, China cooled, and suddenly “scarcity” looked a lot like “inventory management".

The funniest part is that the industry’s preferred definition of “recovery” is “we’re sold out again”. Watchmakers don’t want you to be able to buy what you want when you want it. They want you to want what you can’t buy, because the wait is the marketing. Rolex even managed to sell fewer units (Morgan Stanley/LuxeConsult estimate volumes down 2% to 1.1m) while growing value via higher average selling prices, which is the most Rolex thing imaginable. If demand softens, just become more Rolex-y... 🫠

Concluding, maybe you can get one now, but the whole equilibrium of luxury watches is that availability is a temporary market glitch, and the “healthy” state of the system is a boutique employee telling you politely that your money is not sufficient.... you also need time. Bloomberg

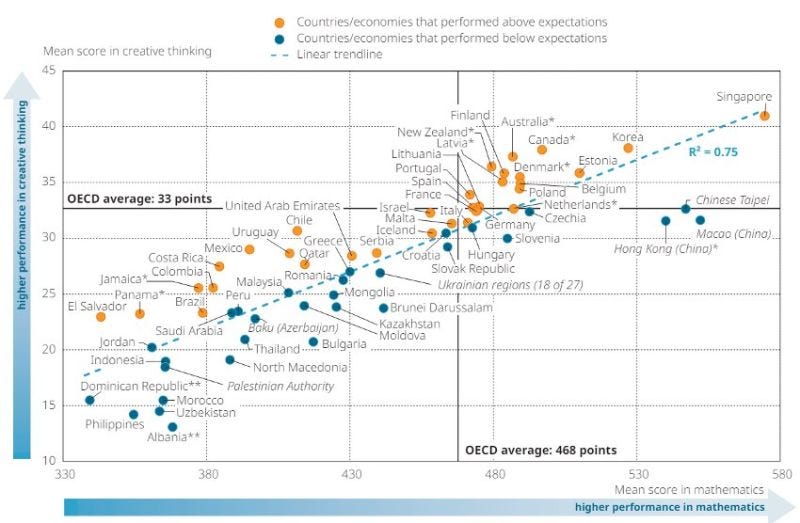

New date from PISA tests. To think outside the box, you need to ‘put’ in the box

This chart is a great example of how reality keeps ruining everyone’s preferred narrative. Because a lot of people want the story to be: “Math is rigid, creativity is free, and if you make kids do too many equations they’ll never write a novel". And PISA is like: actually, the countries where students score higher in math also tend to score higher in creative thinking (!).

Hence, we can conclude that “rigor is a creativity hack”. If you can reason precisely, hold multiple constraints in your head, and grind through a hard problem without panicking, you can also write fiction with structure, draw a poster that communicates, and come up with original solutions under rules.

Creativity is competence within constraints. Also, rich countries do better at school in general, so this might just be “well-funded systems produce broadly capable kids”. But either way it’s a nice reminder that “creative” doesn’t mean “vibes-based”, but it means you have enough mental horsepower and discipline to play, recombine, and still land the plane.

on Shopify 🛍️

Once you see Shopify as a protocol rather than a store builder, the strategy makes more sense, which is, let Amazon own its walled garden, let social platforms fight over impulse clicks, and focus instead on owning the identity, payments, and data pipes that sit underneath millions of independent merchants, because if the next wave of AI agents are the ones choosing where we buy, the platform that already runs those rails is in a much better position than the one that just rents out a storefront. WIMM

on Spotify 🎶

The interesting thing about Spotify’s AI push is that they’re quietly turning a historically terrible business (licensing the same catalog as everyone else) into a data-compounding machine where every marginal listener makes the product better for everyone else.

If you view Spotify as an AI-scaling experiment, the logic flips. Labels own the songs, but Spotify owns the behavioral exhaust, which is exactly what you need to build hyper-targeted discovery, performance ads, and eventually agents that decide what you hear next on your behalf. At that point, the catalog is a commodity input and the real asset is the model that sits between artists and ears, which is why the earnings call matters less for “premium vs. ad-supported ARPU” and more for how fast Spotify can turn its listening graph into an AI-native distribution monopoly. WIMM