(#168) The SaaSpocalypse is a pricing problem

The Tinder-ization of the job market

I consider “Where is my MOAT?“ to be like a mini-MBA 😎

This week, my subscribers receive 4 posts. Here’s the schedule for this week:

12 March - [Analysis] on the Middle East and some implications

13 March - [Essay] Workflow ownership is the next platform war.

14 March - [Deep dive] - Mastercard

15 March - [Deep dive] - Adobe

…and here is the schedule for the next week:

18 March - opening my 3rd portfolio (for Premium/paying subscribers only)

19 March - [Essay] Lessons from Koenigsegg

20 March - [Analysis] The disruption of the German car industry

21 March - [Market updates] Oracle

22 March - [Deep dive] Micron

If you find WIMM useful, please share it with a friend or a colleague. WIMM is free for one month ... plenty of time to decide if it’s worth keeping in your stack.

Dear OnStrategy Reader,

Here is what you will find in this issue:

The SaaSpocalypse is a pricing problem

The dealer moat strikes back 😎

Gen Z and risk

on Koenigsegg ...and the long road to IPO

The Tinder-ization of the job market

on the Middle East 🛢️

…and much more

Onto the update:

The SaaSpocalypse is a pricing problem

The SaaS boom created a peculiar economic machine where companies sold tools that helped other companies build software, manage work, track tickets, and coordinate teams, and they priced those tools per seat. As long as headcount kept growing, revenue did too. AI quietly breaks that equation. If AI allows a team of 10 engineers to do the work that previously required 15, then the customer’s productivity rises while the SaaS vendor’s seat-based revenue shrinks. That dynamic sits behind the recent layoffs at Atlassian and the broader sell-off in software stocks, where investors suddenly realized that the same technology promising productivity gains for customers may compress demand for the very tools those customers buy. The SaaS model assumed that knowledge work scaled with people; AI suggests that knowledge work might scale with compute instead.

This is why the so-called “SaaSpocalypse” feels less like a cyclical downturn and more like a structural shift. If AI agents can perform tasks that previously required humans clicking through dashboards, the center of gravity moves from workflow software to automation layers. In that world, the winners look less like traditional SaaS vendors selling seats and more like platforms selling outcomes. Atlassian’s layoffs signal something deeper than cost-cutting. They are an attempt to reposition the company for a world where software is no longer just a tool for workers but a substitute for them. The paradox of AI SaaS is that the better it works, the fewer users you need. And when your pricing depends on users, success starts to look suspiciously like disruption.

Most SaaS should go private and fix their go-to-market pricing strategy. Few will do, and many will fail/stagnate (=become semi-irrelevant). FT

The dealer moat strikes back 😎

Volkswagen’s Scout gambit is basically a corporate-law version of a spin move. That is, take a century-old car company, wrap a new electric-and-hybrid truck brand around it, and then try to sneak past the dealer network by saying, more or less, “this one is different.”

Dealers, naturally, are reacting as though VW has announced a pilot program to repossess their margins... and in a way, it has. Direct-to-consumer is not really about vibes or modernity or even customer experience, though everyone says those words a lot. Actually, it is about owning pricing, data, software updates, financing, service relationships, and all the lovely recurring economics that used to get diluted across a franchise system.

The dealer argues that they protect consumers through competition and service. The Scout argument is that consumers hate buying cars and would prefer a cleaner, more controlled experience. Both are true, which is what makes this fun because the real fight is over who gets to intermediate trust.

If Scout wins, every legacy automaker will be tempted to invent a “new brand” and declare independence from its own distribution. If the dealers win, they will have demonstrated that in America, the most durable moat in autos may not be manufacturing or software, but a state-by-state legal regime built to ensure that nobody, under any circumstances, gets to buy a car too efficiently. WSJ

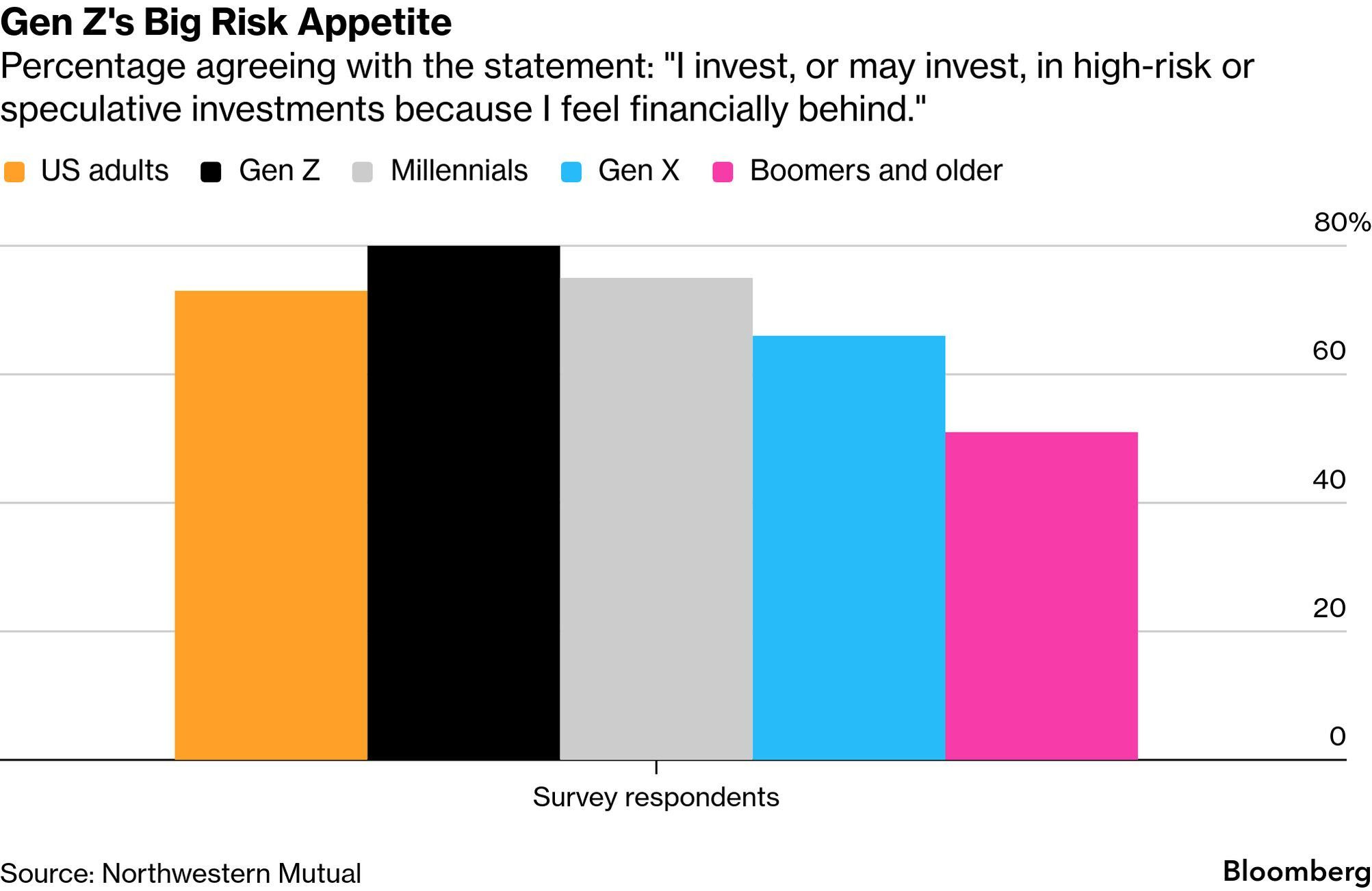

Gen Z and risk

There is a theory of investing that says you should steadily save, buy diversified index funds, and wait 40 years. There is another theory that says if housing is unaffordable, wages are flat, and you feel financially behind at age 23, then the rational portfolio is “whatever might 10x by Friday” 🫠

(not financial advice ❗️)

Unsurprisingly, a growing share of Gen Z seems to prefer the second strategy, putting money into prediction markets, sports betting, crypto, and other high-variance assets because they believe those bets can get them to their goals faster. If you think the normal financial ladder is broken, the optimal strategy is not patience, but volatility.

In that sense, “financial nihilism” is less about recklessness and more about portfolio theory applied to despair. When the baseline outcome looks bad, maximizing upside starts to look perfectly rational. Bloomberg

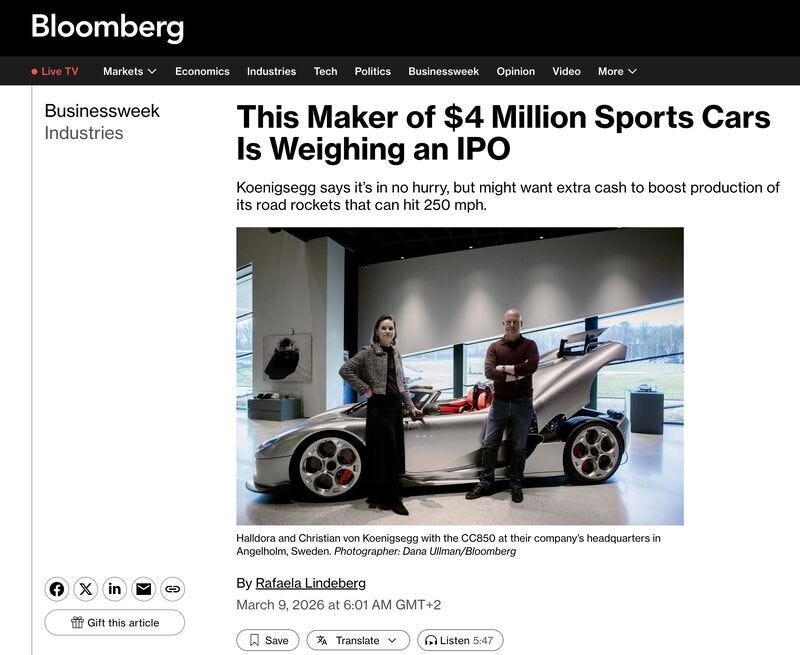

on Koenigsegg ...and the long road to IPO

Koenigsegg is interesting because it sits at the intersection of two very different business models: luxury and technology. On one hand, the company is a classic scarcity-driven luxury brand (ie. producing only a few dozen hypercars per year priced between roughly $2.8 million and $4 million, with production planned to rise only to about 150–200 units annually).

That naturally invites comparisons to Ferrari or Hermès, where the core asset is not manufacturing scale but brand, exclusivity, and pricing power.

On the other hand, Koenigsegg behaves more like a deep-tech startup. It develops its own engines, transmissions, batteries, and engineering innovations internally, which means the intellectual property, not the number of cars produced, may ultimately be the real moat. Bloomberg

The Tinder-ization of the job market

The “Tinder-ization” frame is right because the labor market has quietly shifted from matching to swiping. AI makes it almost free for candidates to generate 200 tailored applications and almost free for employers to ingest 20,000 resumes, so both sides rationally do more of the thing that feels like progress (apply, filter) and less of the thing that actually is progress (talk, decide).

The result is congestion. The pipe gets wider at the top and narrower at the bottom, and the scarce resource becomes human attention at the point of commitment. That’s why the weird macro pattern shows up in the hiring rate rather than unemployment. People still have jobs, but fewer people are getting new jobs, because everyone is trapped in an infinite scroll of “maybe".

The implication is that hiring becomes a marketplace with adverse selection and spam dynamics, which pushes everyone toward gatekeeping and brands. Employers respond with harder screens, more rounds, more referrals, and more “signals” that reduce volume (pedigree, prior employers, internal networks). Candidates respond by optimizing for ATS keywords, prompt-engineering cover letters, and leaning even harder on warm intros, because when the funnel is flooded, relationships become the only filter that still works.

In other words, AI doesn’t end work, but it turns hiring into a platform problem, where the winners are the ones who control distribution (recruiters with networks, companies with reputations, candidates with social capital), and everyone else is stuck swiping. LINK

on the Middle East 🛢️

In my latest Where is my MOAT? analysis I argue that what’s happening in the region is a live stress test of the entire post-Cold War risk map: oil flows weaponized, Dubai and the Gulf countries doing damage control as financial hubs, shipping lanes repriced by drones and missiles, and airlines, tourism, and defense stocks quietly rerating around a new baseline of fragility.

I walk through how a real disruption in Iranian supply or the Strait of Hormuz would transmit into energy, FX, inflation and equities, which sectors are accidental losers and surprise winners, and what this all means for a long-term portfolio that has to live with more frequent regional shocks and less global redundancy. WIMM

[Essay] Workflow ownership is the next 'Platform War'

For two decades, enterprise software competed to become the system of record. Salesforce wanted to own the customer record. Workday wanted to own the employee record. SAP wanted to own the operational record. In the AI era, that battleground is shifting. The next war will not be won by the company that merely stores the data. It will be won by the company that does the work. Or, more precisely, the company that becomes the operating layer through which a professional’s judgment, sequence of actions, approvals, exceptions, and institutional habits actually flow. That is workflow ownership and it is the next platform war.

This is the key mistake in much of the current debate about whether AI will “eat” application software. That framing is directionally right but analytically incomplete. AI will absolutely compress interfaces, reduce the value of brittle menu-driven UX, and make it easier to rebuild surface-level functionality. But that does not mean software disappears. It means the basis of advantage moves down one layer, from screens and forms to orchestration, reasoning, and embedded process. As Steven Sinofsky argues, AI changes what we build and who builds it, but not the amount of software the world needs. In fact, paradigm shifts historically create more software, not less. Here is the Jevon’s paradox in real life (from Citadel Securities). WIMM