(#169) OpenAI has a strategy; SAP has changed its business model; and Pinterest's options

The AI Capex shock (and two implications)

I consider “Where is my MOAT?“ to be like a mini-MBA 😎

This week, my subscribers receive 5 posts. Here’s the schedule for this week:

18 March - [Essay] Lessons from Koenigsegg

19 March - [Analysis] The disruption of the German car industry

20 March - [Market updates] Oracle

21 March - [Deep dive] Micron

22 March - opening my 3rd portfolio (for Premium/paying subscribers only)

…and here is the schedule for the next week:

25 March - [Essay] on business models: B2B vs. B2C (with a focus on OpenAI)

26 March - [Analysis] Macroeconomics (March 2026)

27 March - [Market updates] NVIDIA

28 March - [Deep dive] Reddit

29 March - [Deep dive] Coinbase

If you find WIMM useful, please share it with a friend or a colleague. WIMM is free for one month ... plenty of time to decide if it’s worth keeping in your stack.

Dear OnStrategy Reader,

Here is what you will find in this issue:

OpenAI has a strategy

on SAP’s strategy in an AI world

on the German car industry 🚘

on Pinterest’s options

Refining is the bottleneck

The AI Capex shock (and two implications)

Lessons from Koenigsegg

Onto the update:

on SAP’s strategy in an AI world

SAP’s shift from subscriptions to AI consumption pricing is a redefinition of what enterprise software is, from static systems of record to dynamic systems of work. Subscriptions made sense when value was tied to access, but now consumption makes sense when value is tied to outcomes (i.e., how much work the AI actually does).

As part of the pivot, the company will also create "forward deployed engineering"🫠. SAP is acknowledging that in an AI world, the product is not the software itself, but the integration of that software into the customer’s workflow. That looks less like selling licenses and more like embedding capability, which is precisely where defensibility lives.

The competitive pressure explains the timing. As AI-native players push into enterprise workflows, incumbents can no longer rely on switching costs alone. They need usage-driven value that compounds over time. Consumption pricing aligns SAP with customer ROI, but it also introduces volatility, where the revenue becomes tied to actual usage, which in turn depends on how effectively SAP’s AI is adopted.

In that sense, this is a high-conviction move. SAP is effectively betting that it can move up the stack from infrastructure and data into execution. If it succeeds, it deepens its moat, if not, it risks becoming just another backend provider in someone else’s AI-driven workflow. Bloomberg

on the German car industry 🚘

In my latest Where is my MOAT? analysis I argue that the crisis of the German auto industry is architectural.

For decades these companies dominated the mechanical stack (ie. engines, transmission, precision manufacturing, dealer networks, brand prestige) and then the basis of competition shifted toward batteries, software, power electronics, and supply-chain control, where China moved faster and Tesla rewrote the rules.

The real post-mortem is that German incumbents kept optimizing for a world in which engineering excellence at the component level was enough, just as the industry was becoming a systems business defined by energy, code, and speed of iteration. WIMM

OpenAI has a strategy

Good news: OpenAI has a strategy

Bad news: OpenAI has (only now) a strategy

What looks like a product decision is actually a business model correction. OpenAI is moving from “frontier lab with many bets” to "enterprise software company with a core wedge", and that wedge is (a) coding and (b) productivity. The reason is straightforward. AI only becomes durable when it is embedded in workflows that customers will pay for repeatedly, not when it is spread across consumer experiments that are impressive but hard to monetize.

In that sense, Anthropic’s focus is less about better technology and more about better positioning. Owning the developer and enterprise use case means owning the budget, which in turn funds the compute, which in turn sustains the model lead.

Short reminder: compute is the real scarce resource, strategy becomes allocation and a very “side project” is not just a distraction, but a misallocation of GPUs. In the pre-AI world, companies could afford parallel bets because the marginal cost was people. In the AI world, the marginal cost is infrastructure, which forces focus.

OpenAI’s shift is therefore more about necessity. In a market where the winners are those who best convert compute into revenue, the company that aligns its product surface with monetizable workflows will be the one that can afford to keep training the next generation of models. WSJ

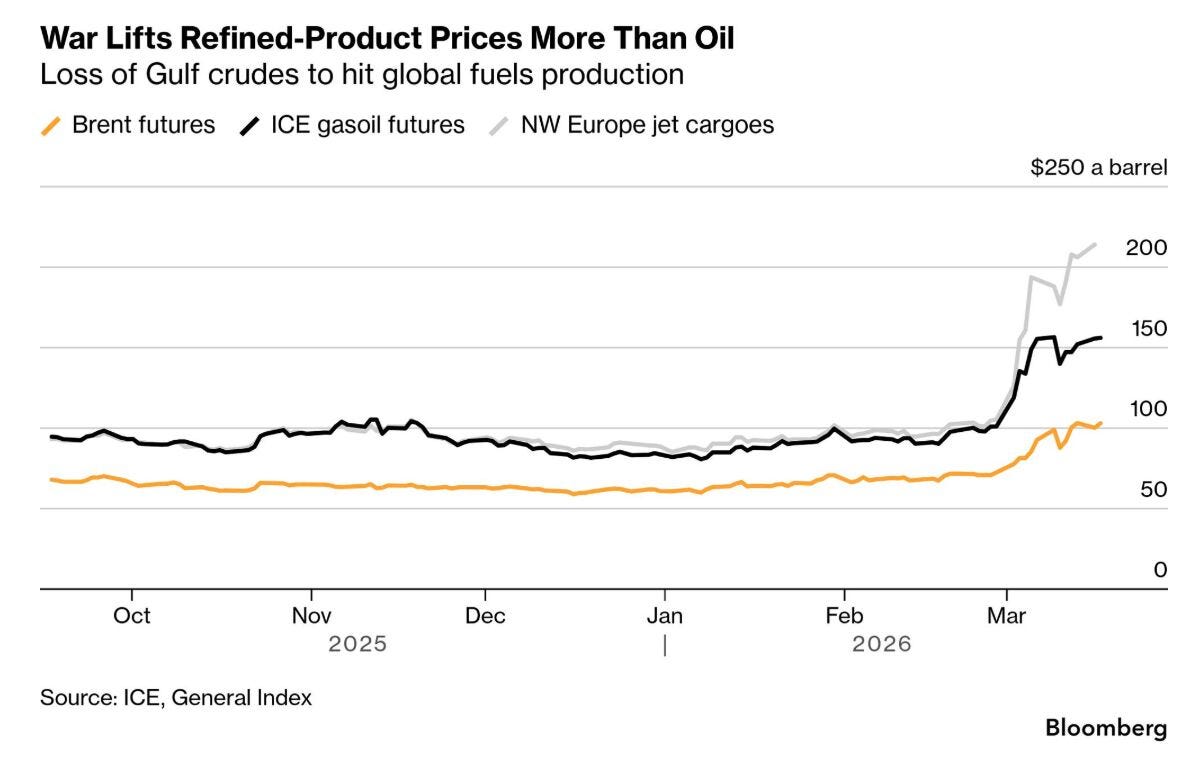

Refining is the bottleneck

What’s interesting here is that oil isn’t really the story, but refining is. You have Brent going up because of geopolitical risk, sure, but refined products (diesel, jet fuel) are going up more, which is the market’s polite way of saying “we don’t just have a supply problem, we have a processing bottleneck".

When infrastructure gets hit and shipping through places like Hormuz becomes “conditional”, you’re short the ability to turn crude into usable fuel, and that’s where prices really gap out.

In other words, wars make complexity expensive. The marginal barrel is no longer about extraction, it’s about logistics, insurance, routing, and refining capacity, all the boring middle layers that suddenly become very exciting when missiles start flying. Crude is the headline, but margins are the trade, and somewhere a refiner is having a very good quarter while airlines, chemicals, and basically anyone who needs actual fuel (as opposed to theoretical barrels) discovers that the real price of energy is not the oil, but it’s everything that happens after. Bloomberg

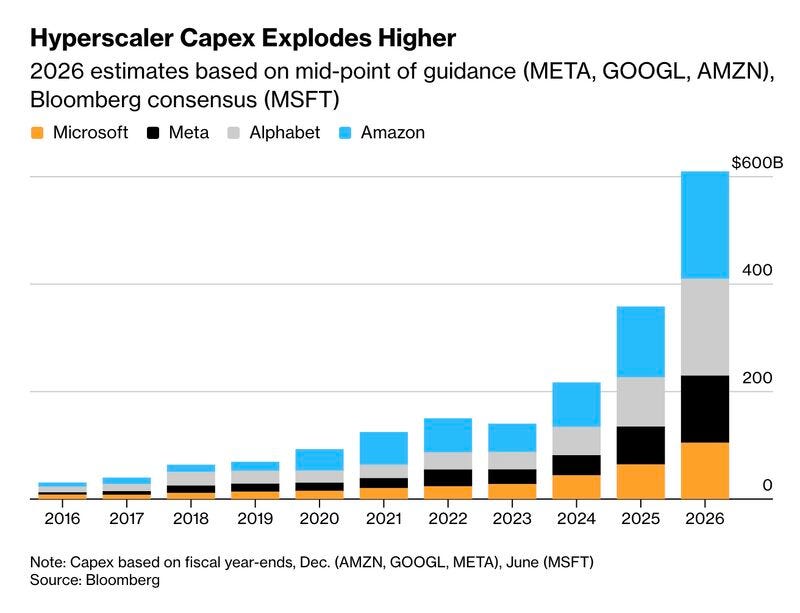

The AI Capex shock (and two implications)

1/ The tech industry is transforming from a labor-heavy business into a capital-heavy one. In the pre-AI era, scaling meant hiring engineers, product managers, sales teams, etc. That meant that people were the bottleneck. In the AI era, scaling means GPUs, power plants, and data centers. And once companies commit to that level of capital expenditure, the market will demand operating leverage somewhere else. That “somewhere else” is labor.

2/ This is why layoffs are not a temporary correction but a structural shift. If the marginal unit of output is now compute rather than human effort, then organizations optimized for hiring thousands of employees suddenly look inefficient. The same companies that once hired aggressively to remove organizational bottlenecks are now discovering that AI agents remove those bottlenecks directly, collapsing layers of coordination and decision-making.

Investors who tolerate hundreds of billions in infrastructure spending will simultaneously expect higher margins, which means fewer humans in the loop. The paradox of the AI boom is therefore that the biggest investment cycle in tech history will coincide with a wave of job cuts, not because companies failed, but because AI changes the production function of software itself. Bloomberg

on Pinterest’s options

Pinterest has the kind of asset that looks magical in a deck and frustrating in a P&L with 600 million users, 80 billion searches, and a user base that often shows up already in shopping mode.

The problem is that Pinterest sits too early in the funnel. It captures inspiration, while Meta, Google, and Amazon are better at capturing transactions. That is a dangerous place to be in digital advertising, because intent without conversion tends to get monetized by someone else.

That is why a sale makes strategic sense. Pinterest looks less like a standalone ad-tech winner and more like an attractive missing piece for a larger platform, especially one that is strong at commerce but weak at discovery. Amazon or Walmart could use Pinterest to move upstream in the shopping journey, while a financial buyer could take advantage of the low valuation and fix the business outside public markets. Pinterest needs an owner who knows how to turn ideas into checkouts. FT

Lessons from Koenigsegg

Excerpt from the esssay:

There is a framework that clarifies much of what is happening in the global economy right now, and it is deceptively simple. In nearly every industry, value is accruing at the extremes. Either you sell something indispensable to billions of people at a price they barely notice, or you sell something irreplaceable to a handful of people at a price high enough to be considered a rarity. Everything in between, the competent, the adequate, the merely good, is being systematically destroyed.

This is not a prediction. It is already happening.

The forces doing the destroying are familiar. Chinese manufacturers, backed by industrial policy (= enormous subsidies at each step of the manufacturing process), cheap energy (hello, USA!), and ruthless supply chain integration, have demonstrated an unmatched ability to manufacture at scale and price commodities toward zero. American technology platforms, powered by abundant and increasingly cheap energy (ie. natural gas, now solar, soon nuclear), run the world’s most valuable software businesses from a position of structural cost advantage. When these two forces converge on a product category, the middle collapses. What survives is either the commodity, which wins on price, or the icon, which wins on meaning.

Europe, in this reading, faces an existential strategic choice. Its labor costs preclude commodity competition. Its regulatory environment complicates the kind of software-driven winner-take-all scaling that produces trillion-dollar American platforms. What remains, what Europe has always, arguably, done best, is craft, expertise, and the particular kind of trust that accumulates over generations. Nasim Taleb calls these “medieval artisanship”. Hermès. LVMH. Porsche, and, sitting at the most interesting extreme, Koenigsegg, which is selling cars between $2.8-4 millions each. (read full essay)