(#171) on the SpaceX IPO 🚀; on inflation 📈

Where does the value accrue in AI?

Dear OnStrategy Reader,

Here is what you will find in this issue:

on the SpaceX IPO 🚀

Where does the value accrue in AI?

How Waymo works

on Social Media ban for youngsters (< 16 yrs)

on inflation 📈

[ESSAY] on AI needs consultants 🧑🏼💻👩🏼💻

Onto the update:

on the SpaceX IPO 🚀

SpaceX going public at a rumored $1.75tn valuation and $75bn raise is, on one level, a financing event and, on another, a queue-jumping event. The market right now is basically a finite pool of excitement, liquidity, passive flows, and tolerance for heroic narratives, and SpaceX seems to have decided that if there is a window, it should go through it first and largest.

That makes sense. If you know that OpenAI and Anthropic are somewhere behind you in the IPO line, you do not politely wait your turn, but you run onto the runway with rockets, satellites, Starlink cash flows, an xAI tie-in, and a valuation so large it makes normal IPOs look like bake sales.

It also helps that the exchange rules have just become friendlier to giant newly public companies, with faster index inclusion and looser float requirements, which is a very elegant way of saying ...“come public fast, sell a tiny slice, and let passive money do some of the work".

The other thing about doing it now is that “now” may be better than “later”. Economic conditions feel like they are deteriorating quickly, and mega-IPO markets are open right up until the moment they are not. If you are Elon Musk and friends, the rational move is to extract the money while the story still clears at maximum altitude, before macro conditions worsen, before rates or risk appetite shift again, and before the next great AI float sucks oxygen out of the room.

There is also a nice bit of financial engineering here. Float less than 5%, maybe let insiders sell on day one, get potentially pulled into the Nasdaq 100 quickly, and create immediate demand from index-linked funds. That is turning market structure into a distribution channel. In other words, SpaceX is not merely doing the biggest IPO in history. It is trying to do the biggest IPO in history before history gets more crowded and more expensive. FT

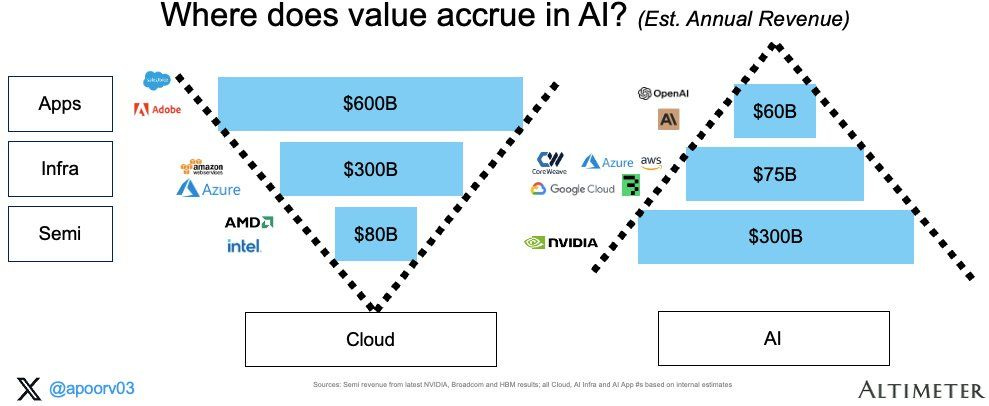

Where does the value accrue in AI?

The fun thing about this chart is that it looks like a classic “apps win in the long run” story, except we are very much not in the long run yet, and in fact the opposite is happening. All the money is sitting at the bottom of the stack, with semis hoarding something like 70% of revenue and even more of the profits, which is a polite way of saying that if you want to get rich in AI, you should sell very expensive shovels to people who think they are digging for gold.

And everyone knows this, which is why the hyperscalers are spending hundreds of billions on capex, partly to build products, but also partly to avoid paying NVIDIA forever, which is not a great long-term business strategy if you are, say, a trillion-dollar company that does not enjoy being someone else’s customer.

But also this is sort of how every platform shift starts: the infrastructure layer gets paid first, the application layer gets paid later, and in the middle there is a lot of venture capital explaining that this time will be different. Maybe it will be, but right now the economics are stubbornly inverted, with apps growing fast in percentage terms but still tiny in absolute dollars, which means that the big strategic question is not “who has the best AI app?”, but “who can escape the tax imposed by compute?” and until that changes, the real business model of AI is less about intelligence and more about electricity, chips, and the willingness of large companies to spend enormous amounts of money today in the hope that someday, somewhere up the stack, someone will figure out how to actually make it back.

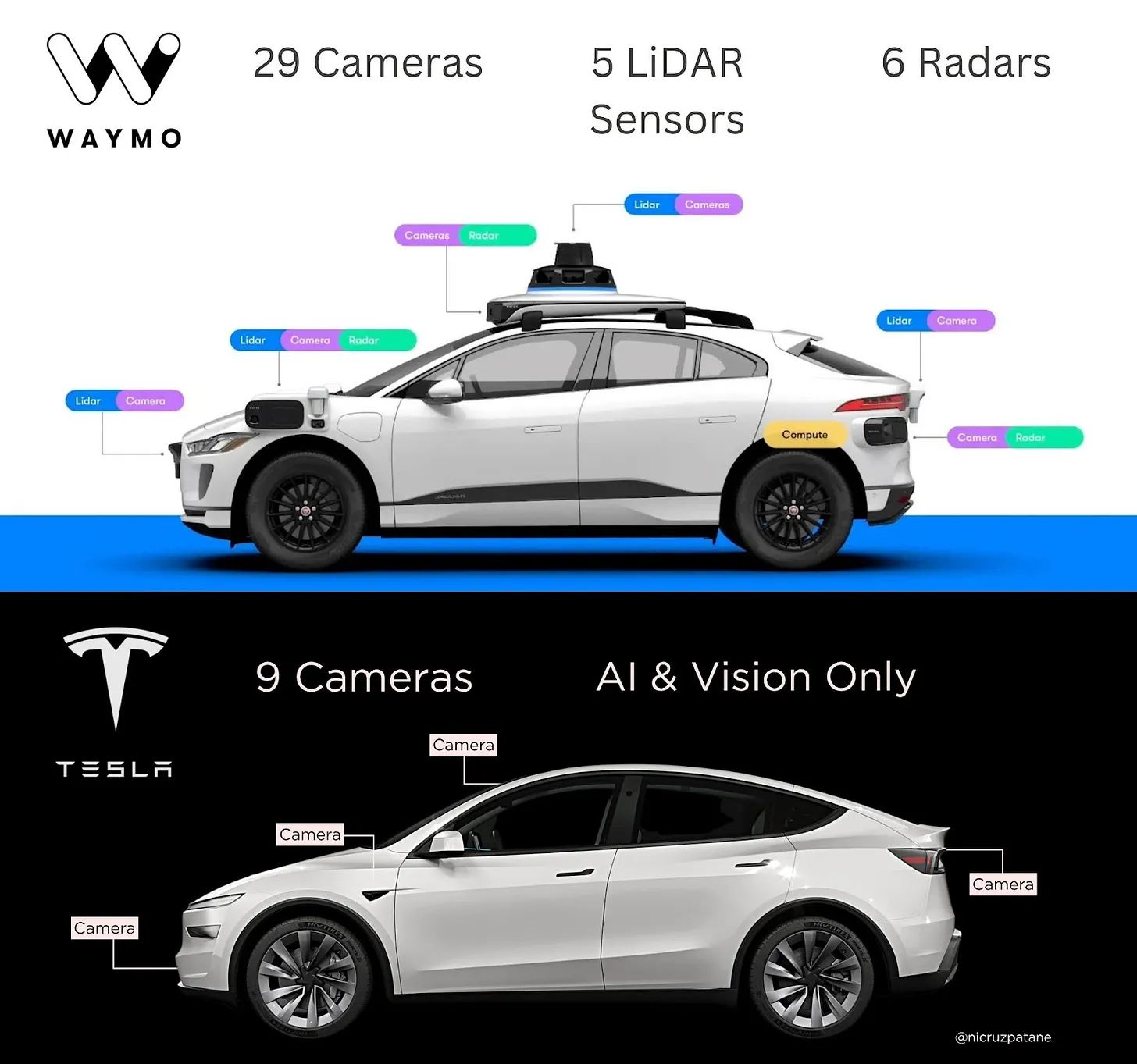

How Waymo works

In my latest essay, I argue that Waymo’s real lesson was about strategy under deep uncertainty. Some problems do not yield to iteration, because they have a minimum investment threshold below which you are simply not solving the same problem.

Waymo won by treating full autonomy as a distinct category from driver assistance, building “the Driver” as a platform rather than a feature, and spending two decades de-risking the stack until it could generalize across cities instead of merely performing well in a demo zone.

The broader point is uncomfortable but useful for executives. When the problem is genuinely hard, the shortcut is often the most expensive path of all. WIMM

on Social Media ban for youngsters (< 16 yrs)

The interesting thing about banning social media for youngsters is that it sounds like a moral argument. Still, it’s actually a market design problem. We built the most sophisticated attention-extraction systems in history and then let the least experienced users compete in them with no safeguards.

These platforms are optimized for engagement, not well-being, which means the equilibrium outcome is predictable (ie. more time spent, more dopamine loops, less focus, worse mental health). Now, saying "let kids use it responsibly" is a bit like saying "let them trade derivatives responsibly", technically possible, empirically unlikely.

If you look at that map, what you’re seeing is governments slowly realizing that the default settings of the internet are misaligned with developmental (mental) needs, and that the cost of inaction compounds over time.

Limiting access is about sequencing it; there is an age for learning algebra, and there should probably be an age for algorithmic feeds too.

Yes, I'm in favour of the ban! Bloomberg

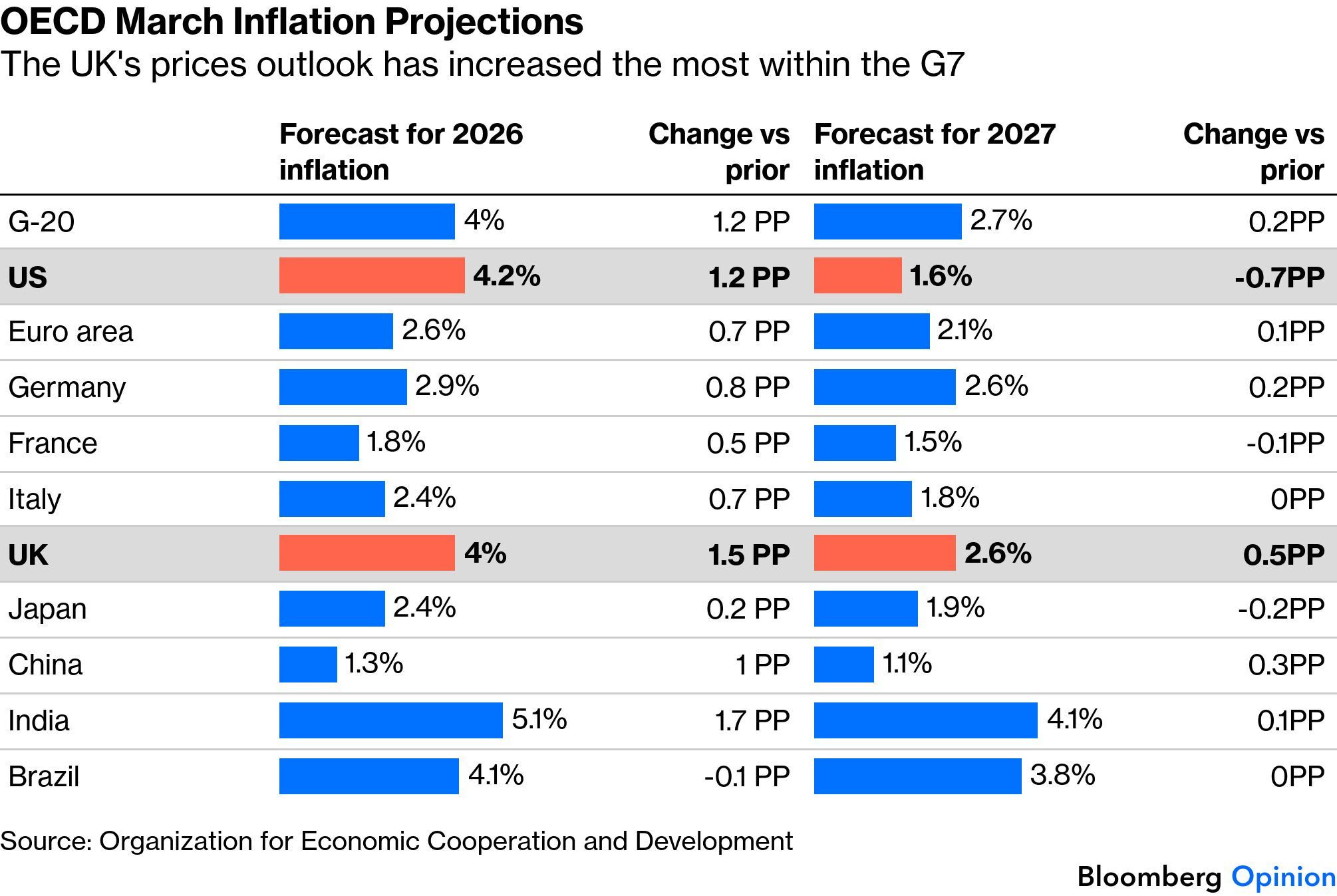

on inflation 📈

What’s striking about this chart is not the level of inflation, but the revision. Inflation is being repriced upward in real time, and the UK stands out as the most sensitive node in that system.

That tells you something structural, which is...exposure. Economies that are more dependent on imported energy and global trade flows are effectively “levered long” geopolitical stability, and when that breaks, their inflation moves first and fastest.

The recent Iran conflict, which has disrupted oil flows (and other byproducts) and pushed energy prices sharply higher, acts as a classic external shock that feeds directly into CPI through fuel, transport, and food costs.

The second-order effect is more interesting. Inflation here becomes a supply chain signal, not just a monetary one. Central banks can manage demand, but they cannot reopen the Strait of Hormuz or stabilize oil infrastructure (20 million barrels were flowing daily from the Middle East). That creates a regime where inflation is both higher and more persistent than expected, while growth weakens (i.e., a mild version of stagflation).

In that world, the dispersion across countries matters more than the average. India and Brazil can run hotter inflation because of growth dynamics, the US can absorb it with relative resilience, but Europe, and especially the UK, ends up caught between imported costs and constrained policy space.

This is also a reminder of any geopolitical book: secure ASAP your (1) energy and (2) food sources. I guess that many read geopolitical books anymore...especially in Brussels or 10 Downing Street.

[ESSAY] on AI needs consultants 🧑🏼💻👩🏼💻

In my latest Where is my MOAT? essay, I argue that the AI boom is creating a surprisingly old-fashioned winner, which is, the person who actually shows up and makes the thing work.

Models are getting cheaper, more available, and more impressive, but that mostly means the scarce asset shifts from access to implementation (ie. redesigning workflows, reassigning decision rights, training teams, setting guardrails, and measuring whether any of this improves outcomes rather than just producing a nicer board deck).

In other words, the real moat in enterprise AI may not belong to the lab with the smartest model, but to the companies and advisors who become the translators between generic capability and messy organizational reality.

This week in “Where is my MOAT?”:

2 April: [Essay] AI needs consultants

3 April: [Market updates] ARM

4 April: [How startups work] Waymo —> new category to WIMM

5 April: [Deep dive] on Intel