(#172) 📉on mega IPOs; 🤖 on Perplexity and 🍏Apple at 50

[Analysis] Winners and losers in the memory shortage

Personal update 🤓

I did not particularly expect to become a certified investment consultant....and yet, here we are.

What started as writing several times a week on Where is my MOAT? gradually became something bigger:

a way of thinking about businesses, markets, incentives, technology, commodities, and...

capital allocation that is a bit more structured than “buy this” or “sell that”

Markets, after all, are rarely just about price targets. They are about business models, power, scarcity, timing, management quality, regulation, second-order effects, and the inconvenient fact that everything connects to everything else.

After publishing 4-5 times a week, I realized I had built something like an MBA niche for investors. Not the generic kind, but the “skin in the game” useful kind. The kind that helps you understand why a company matters, what could change its moat, how commodities shape industries, and how all of this affects the decisions you make with your own capital.

I’m officially certified as an investment consultant, and I now work with people in three ways:

1/ on a one-time basis

2/ on a monthly basis, or

3/ through tailored investment education and advisory support that companies can offer as a benefit to employees or clients.

Send me a message to work together.

👉 Find all details here: https://whereismymoat.com/work-with-me

Dear OnStrategy Reader,

Here is what you will find in this issue:

on Perplexity

[Analysis] Winners and losers in the memory shortage

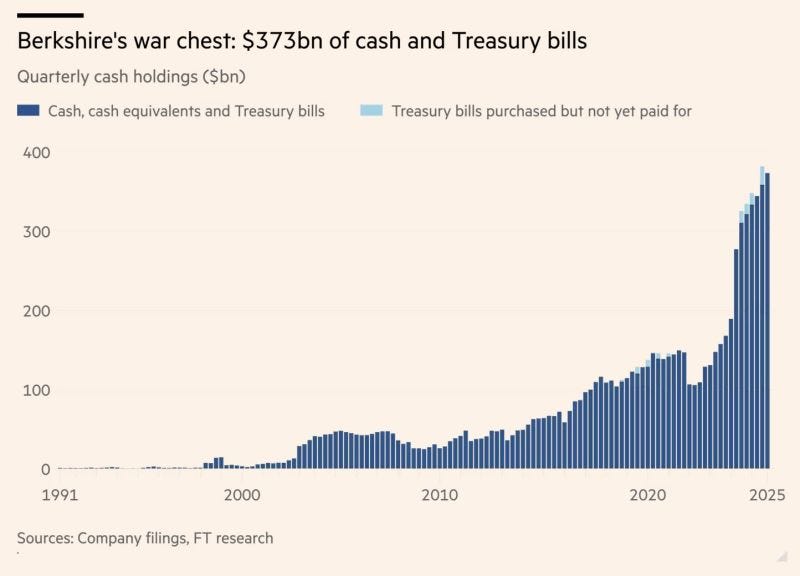

Berkshire Hathaway has $373 billion in cash

on the middle management 🧑💼👩🏼💼

on mega IPOs: SpaceX, OpenAI and Anthropic

on Intel

[Essay] Apple at 50

Onto the update:

on Perplexity

Perplexity’s pivot from "search" to "agents" is a recognition that “answering questions” is a feature, while “doing work” is a business model. Search is a brutally difficult market because incumbents own distribution, advertisers subsidize user acquisition, and the marginal answer is easy to compare.

Agents, by contrast, are closer to labor. They consume more compute, but they also create more measurable value, which makes usage-based pricing feel natural rather than forced. That is why the revenue inflection matters. Moving from a search-like interface to a task-completion layer turns Perplexity from a thin wrapper around model access into something more like an intelligent broker of work, routing each request to the most efficient model and capturing margin through orchestration rather than through model ownership itself.

I start to feel more optimistic about Perplexity's future. FT

[Analysis] Winners and losers in the memory shortage

The first and most obvious beneficiaries are the memory manufacturers themselves. Samsung, SK Hynix, and Micron Technology collectively control more than 95% of global DRAM production and the majority of enterprise NAND supply. After suffering through a bruising 2023 downcycle, all three companies implemented aggressive supply discipline, which meant cutting capital expenditure, reducing wafer starts, and delaying capacity expansions. This was a strategy born of survival. The result is that when demand returned with unexpected force (driven largely by HBM - High Bandwidth Memory), requirements for AI accelerators, these 3 players found themselves holding pricing power they had not enjoyed in years. Of course, the market ended like this after decaded of transformation. (continue reading it HERE)

Berkshire Hathaway has $373 billion in cash

Berkshire Hathaway having $373 billion in cash is one of those things that sounds conservative until you realize it is also extremely aggressive, just pointed in a different direction. Buffett is basically running the world’s largest "wait and see" trade, which is funny because most investors feel compelled to always be doing something, whereas Buffett (Greg Abel more exactly) is very comfortable doing nothing at scale....and the scale matters. When you have that much cash you are waiting for everyone else to run out of options first, at which point you become the market.

Also, there is a subtle signal here about the opportunity set. Cash piles this large are not built because there are too many attractive investments, they are built because there are too few that meet the bar. So either Abel has become unusually cautious, or the market has become unusually expensive, or both, which is a slightly awkward backdrop for everyone else who is fully invested and explaining why this time is different.

The nice thing about having $373 billion in cash is that you don't need to be right today, you just need to be right eventually, and preferably at a moment when everyone else wishes they had been a bit more patient.

on the middle management 🧑💼👩🏼💼

The core idea in Jack Dorsey's new essay is that hierarchy is more about bandwidth..not power. For 2,000 years, organizations existed to route information through layers of humans with limited span of control, and everything from Roman legions to McKinsey org charts was essentially an optimization of that constraint.

What changes with AI is not just productivity, but the removal of that bottleneck. If a system can maintain a real-time “world model” of the company and its customers, then the coordination function of middle management becomes software rather than people. That reframes the firm from a collection of teams executing plans to a continuously updating system composing actions, where capabilities are modular and decisions emerge from data rather than being pushed down a chain of command.

The interesting second-order effect is that this turns organizational design into a data problem and a moat problem. The companies that win are not those with the best org charts, but those with the richest, most compounding "world models", built on proprietary, high-signal data like transactions or workflows. That creates a feedback loop where better models drive better decisions, which drive more activity, which enriches the model further. At that point, AI is not a cost-saving tool but a coordination engine that collapses layers and accelerates iteration speed, effectively making “speed of information flow” the new primary competitive advantage.

The risk, of course, is that if your company does not have a unique data advantage, this architecture becomes commoditized, and instead of becoming an intelligence system, you become just another node running someone else’s model.

Anyway, make some time to read his essay. LINK

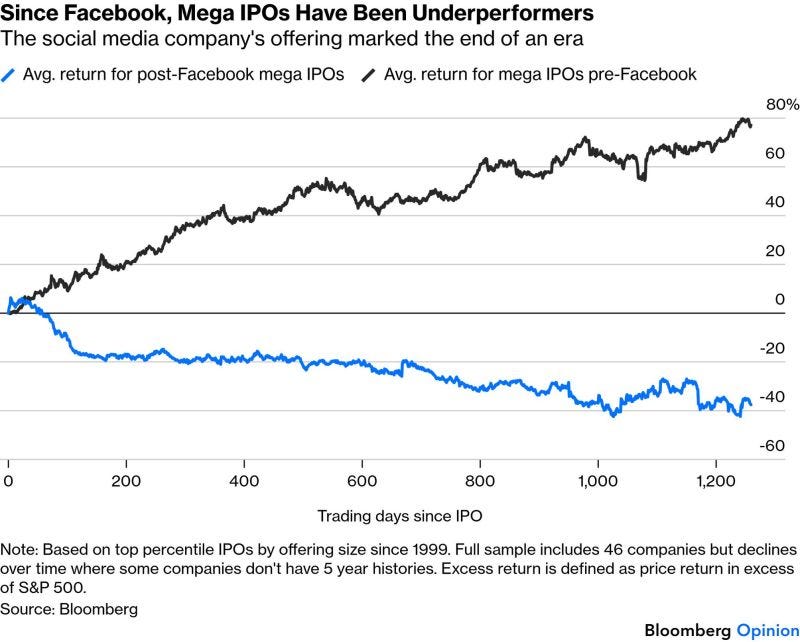

on mega IPOs: SpaceX, OpenAI and Anthropic

The thing about mega IPOs is that they are sold as "once-in-a-generation opportunities", which is usually true in the sense that they generate once-in-a-generation underwriting fees and then, for public investors, once-in-a-generation disappointment.

This chart is basically saying that if you bought the biggest, most hyped IPOs after Facebook, you systematically underperformed the market for the next five years, which is a nice way of saying you paid peak narrative prices for businesses that had already done most of their compounding in private markets. Of course, now we are about to do it again, but bigger, with SpaceX, OpenAI, Anthropic, and friends lining up, which is great because nothing says “healthy market” like a queue of trillion-dollar stories trying to come public at the same time.

Also, there is a nice timing element here, which is that companies tend to IPO when conditions are good for them, not for you, and right now conditions are good in the sense that there is still liquidity, still excitement, and still a willingness to believe that this time the growth curve will justify the valuation.

Here is the hack: if you are the issuer, you might also notice that macro conditions feel a bit wobbly, rates are not exactly friendly, and the window could close, so you accelerate. Which means that what looks like a supply of exciting new public companies is also a demand for your capital at exactly the moment when the risk is highest, and historically that has not been a great trade, even if the companies themselves turn out to be very good businesses eventually. Bloomberg

on Intel

In my latest Where is my MOAT? deep dive, I argue that Intel’s problem is not that it has no moat, but that it has two very different ones living under the same roof:

1/ a still-real CPU franchise built on x86 inertia, enterprise switching costs, and the growing relevance of CPUs in AI orchestration and inference, and

2/ a foundry business that is strategically important but still economically unfinished.

The quarter was better than feared, especially in data center, and management effectively admitted the issue was demand exceeding supply rather than demand collapsing, which is a meaningful change in tone, but the real question is still execution: whether 18A yields improve, supply normalizes, and foundry starts turning milestones into real external customers.

Until then, Intel remains a company with valuable assets and credible strategic optionality, but one whose turnaround still lives more in verbs than in cash flows.

Read the full analysis here.

[Essay] Apple at 50

In my latest Where is my MOAT? essay, I argue that Apple’s real genius over the last 50 years was building the greatest customer-creation machine in consumer tech: 5.1 billion devices shipped, 2.5 billion active devices today, and a services layer now worth $112.8B annually, all reinforcing one another through control of the human-computer interface.

The more interesting question is forward-looking. Apple may be perfectly built for the deterministic era it dominated (ie. polished hardware, controlled experiences, elegant integration), while the next era belongs to probabilistic AI systems shaped by messy data, iteration, and uncertainty, where other companies may be structurally better positioned. [Continue reading HERE]

Thank you for being an onStrategy reader!

Interesting newsletters 💡

Endi Ungureanu - Tura de duminica