(#174) META takes “search”; Allbirds (a shoe company) is now a GPU-as-a-service company 🫠

back on UBER 🚕

Dear OnStrategy Reader,

Here is what you will find in this issue:

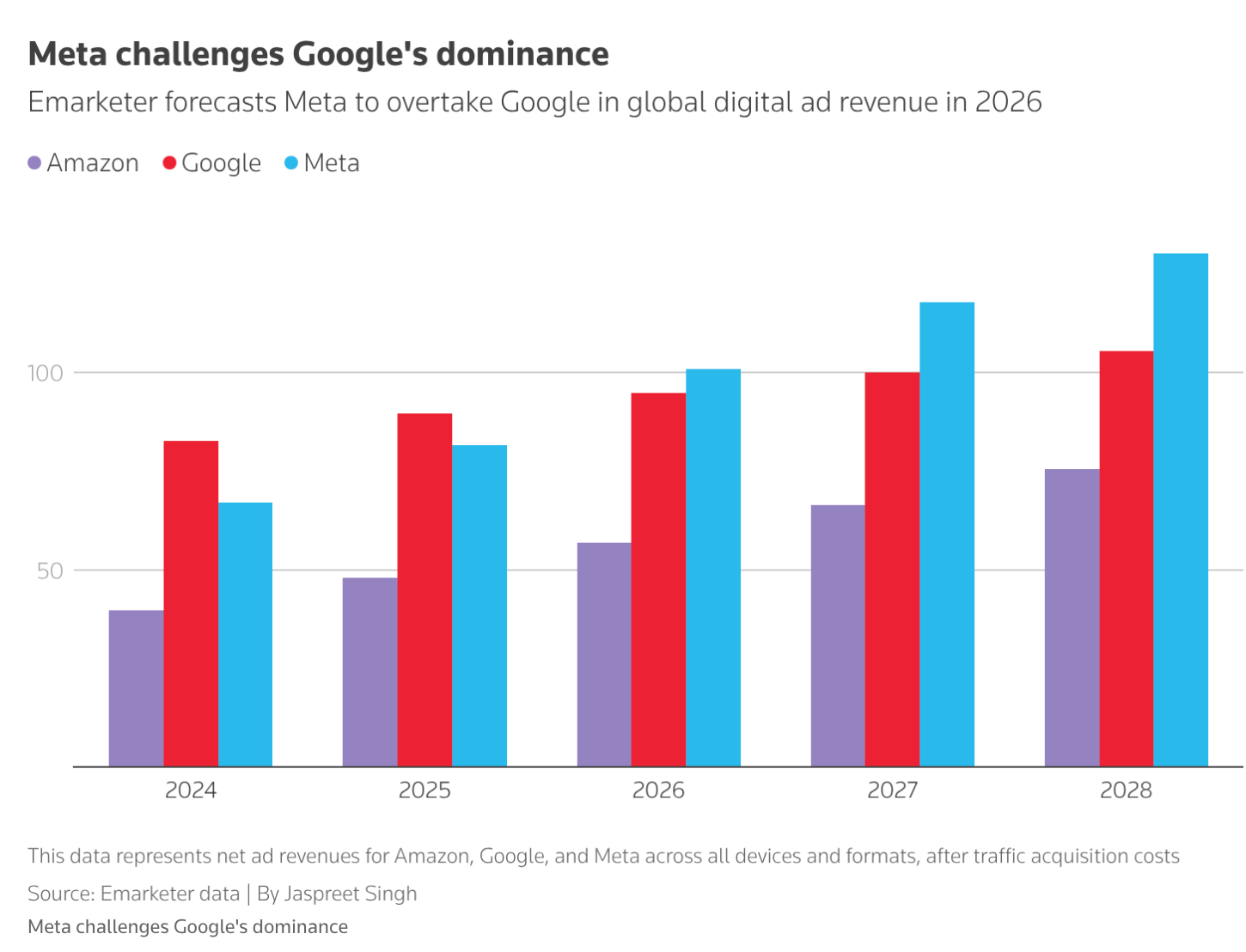

Meta takes “search”

on Allbirds

back on UBER 🚕

Regulation drives innovation away

🍵 Matcha is sooo...yesterday (sort of)

[Essay] The future of company structure

..and more

Onto the update:

Meta takes “search”

What this really means is that the center of gravity in digital advertising is shifting from explicit intent (deterministic) to probabilistic discovery. Google’s great strength was always that users told it what they wanted. Meta’s great strength is that it infers what users might want before they ask. For a long time, search was the more durable business because intent is the cleanest signal in advertising. AI changes that equation. If Meta can use automation and products like Advantage+ to turn its enormous corpus of behavioral data into better targeting and easier campaign execution, then the ad dollar follows performance, not legacy. In that sense, Meta overtaking Google is a sign that the ad market increasingly values prediction over query.

The implications go further.

First, Meta’s expansion across Instagram, Reels, Threads, and WhatsApp means it is becoming more an ad-surface aggregator, with multiple formats capturing different moments of attention.

Second, Google’s diversification is strategically rational but financially dilutive in this comparison. Subscriptions and other businesses may strengthen Alphabet overall, but they also make the ad engine look less singular versus Meta’s pure optimization machine.

Finally, the concentration point matters most. If Meta, Google, and Amazon take well over 60% of global digital ad spend, then the losers is the broader open web. The market is consolidating around the companies with the best data, the best AI, and the largest distribution, and once that loop closes, it becomes very hard to break. Reuters

on Allbirds

This is one of those trades where the business model is “AI”, but the actual product is volatility. Allbirds pivoting from sneakers to GPU cloud is, on its face, absurd, but the financing is extremely rational. You attach a credible buzzword to a listed shell, watch the stock re-rate, and then hand a convertible investor a call option on that re-rating with basically no downside.

The investor isn’t really betting on Allbirds becoming the next Nvidia. They’re betting that the market will believe it might, at least long enough to convert cheap paper into expensive stock and sell it to someone else who likes the story. The clever part is the structure: small upfront capital, optional follow-on, and a conversion mechanism that actually benefits from volatility, which is perfect for a meme-driven market where prices oscillate between “this is the future” and “wait, this was a shoe company” 🫠

Finally, you end up with two parallel realities. In one, Allbirds is building “AI-native cloud infrastructure”, which is a very capital-intensive, expertise-heavy business that it is not obviously equipped to run. In the other, Allbirds is a financing vehicle for harvesting AI enthusiasm, where the real innovation is not GPUs but capital structure.

Honestly, the second one is working great. The deeper implication is that in frothy markets, the fastest way to create value is not to build something new, but to relabel something old and attach the right kind of optionality to it. The only real question is timing. Can you convert and sell before the narrative collapses, or do you end up holding a very ambitious cloud strategy and a warehouse full of wool sneakers? BBC

back on UBER 🚕

Uber’s $10bn pivot into robotaxis is a normal existential hedge. The company built its moat on aggregating supply (drivers) and demand (riders), but autonomy threatens to collapse that supply layer entirely, handing power to whoever owns the fleet and the software. What’s striking is the inversion where Uber, once the archetype of asset-light scaling, is now committing billions to secure access to vehicles and even financing their deployment, effectively trying to remain the interface while conceding control of the core technology. The risk, of course, is that the real winners (Waymo, Tesla, Zoox) have no structural reason to tolerate an intermediary if they can go direct, which turns Uber’s strategy into a race to prove that distribution still matters in a vertically integrated world.

If Uber can remain the demand aggregator, it preserves relevance. If not, it becomes a transitional layer in a stack that is rapidly integrating around it. FT

Regulation drives innovation away

There’s a funny thing about being a “super-regulator”. It works great right up until the moment something actually important happens. Then you discover that the people building the thing are in California, the chips are in Arizona (or Asia), the cloud is in Virginia, and the guest list is…also in the US.

Europe, meanwhile, is left refreshing its inbox waiting for access to a model that can apparently out-hack most humans, while the real decisions are being made in private rooms with companies that actually ship products. It turns out that if your comparative advantage is writing rules after the fact, you don’t get invited to the meeting where the future is decided.

Europe spent a decade perfecting the art of regulating technology it didn’t build, and now it’s trying to regulate technology it can’t even access. The AI Act says “you must comply”, but Anthropic says “you can’t test it”... and, well, those are different kinds of power.

Regulation assumes leverage, but leverage comes from markets, capital, and capability. The US has all three, so it can decide who sees the model. Europe has…process. Which is useful for writing very thoughtful documents about risks, but less useful when the risk is that you’re no longer relevant.

I wrote here, on LinkedIn and in my newsletter, that the EU will eventually get a scrappy internet. Now will get a scrappy AI. POLITICO

🍵 Matcha is sooo...yesterday (sort of)

The fun thing about "ube" is about color arbitrage. You take a perfectly normal beverage category, add a visually distinctive ingredient, and suddenly you can charge matcha prices for something that is, in wholesale terms, cheaper to produce. Which is great, because coffee chains are not actually in the business of selling coffee anymore, they are in the business of selling reasons to walk into a store and post about it on Instagram (prove me wrong 😎)

Matcha worked because it was green and vaguely healthy and showed up well on TikTok, but ube (what a horrivle name!) works because it is purple and shows up even better. If tomorrow there is a bright blue root vegetable, that will probably be next quarter’s strategy.

But also this is a slightly defensive move dressed up as innovation. The big chains are losing share to smaller, trend-native competitors, and when consumer spending is under pressure, the easiest lever is novelty. Launch something limited, make it look good, price it like a premium product, and hope it brings in younger customers who were otherwise going somewhere else. The risk is that novelty is not a moat, it is a treadmill, so you end up in a situation where you are constantly searching for "the next matcha", which is a polite way of saying that the last one already peaked. FT

on “The Great Flattening” & McKinsey & Company

What sits between the lines in the article below is a redefinition of the firm itself. Historically, organizations scaled by adding people to process information, which is why hierarchy existed in the first place. Now, with agents embedded directly into workflows, the coordination layer shifts from humans to software. The implication is flatter org charts, but also a fundamentally different operating model where “teamwork” becomes a mix of humans and agents executing tasks in parallel, with AI continuously synthesizing inputs and pushing decisions forward.

In that world, management is more about designing systems (ie. setting objectives, guardrails, and data flow), while agents handle the execution and increasingly the analysis itself.

The second-order effect is that decision-making becomes ambient. Instead of waiting for reports, meetings, and approvals, the organization is constantly being nudged by AI with “do this", "resolve that", “here are the implications”.... effectively compressing time between signal and action.

This collapses layers not because companies want to cut costs, but because the function those layers served is being automated. The strategic advantage then shifts to companies that can best integrate these signals into their operations. In other words, the org chart gets flatter, but it also becomes dynamic, continuously reconfigured by the flow of information itself. BI

[Essay] The future of company structure

In the AI era, the real question is not whether to organize by function or by business unit. It is where decisions should be made, which capabilities scale best from the center, and where autonomy creates more value than control.

For decades, one of the most consequential choices a CEO could make was deceptively simple: Should the company be organized primarily by function or by business unit? Alfred Chandler’s dictum, structure follows strategy, still holds. Apple’s way of operating is still hard to copy (see How Apple is organized for innovation). But in an era of artificial intelligence, real-time data, and automated workflows, something more fundamental is shifting.

Strategy itself is now shaped by the information architecture a company builds, and the old trade-offs between functional efficiency and business-unit agility are being rewritten. (continue reading)

This week on “Where is my MOAT?”

16 April - WIMM plan (update)

17 April - [Essay] The future of company structure

18 April - [Analysis] Open AI vs Anthropic - deep dive on early data

19 April - [Deep Dive] Johnson & Johnson

Consider subscribing to get that👇🏻 (one month free) —>

Thank you for being an onStrategy reader!

Interesting newsletters 💡

Endi Ungureanu - Tura de duminica