(#177) The globalization of cheap sugar

Google’s Fitbit Air is not really a smartwatch competitor.

Dear OnStrategy Reader,

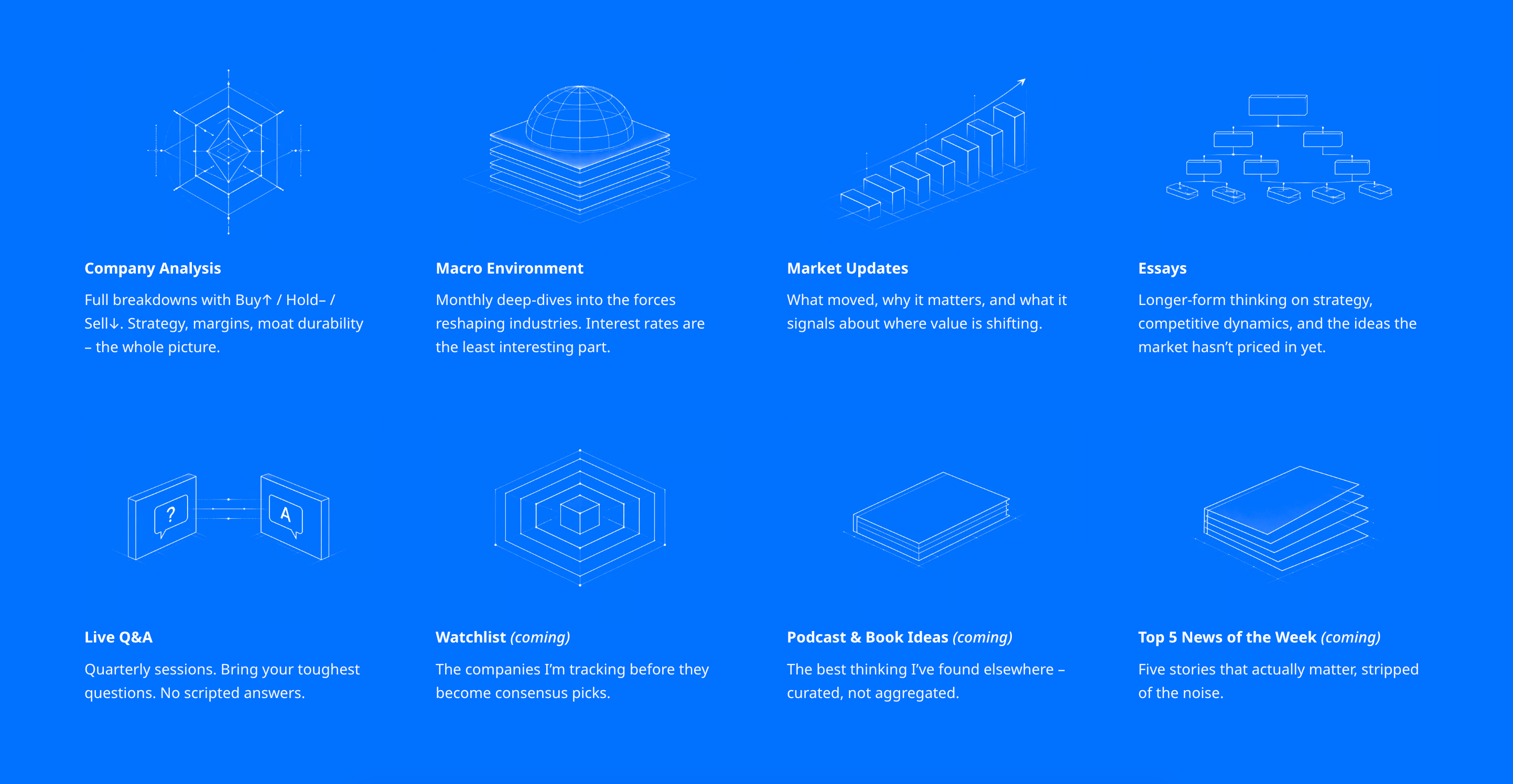

Here is what you will find in this issue:

The globalization of cheap sugar

Google’s Fitbit Air is not really a smartwatch competitor.

The magic of “boring businesses”: pet shops

Amazon Supply Chain Services (ASCS) is the AWS playbook applied to atoms.

Vinted or why people buy second-hand

on Google (Alphabet) & Berkshire Hathaway Q1 earnings

Onto the update:

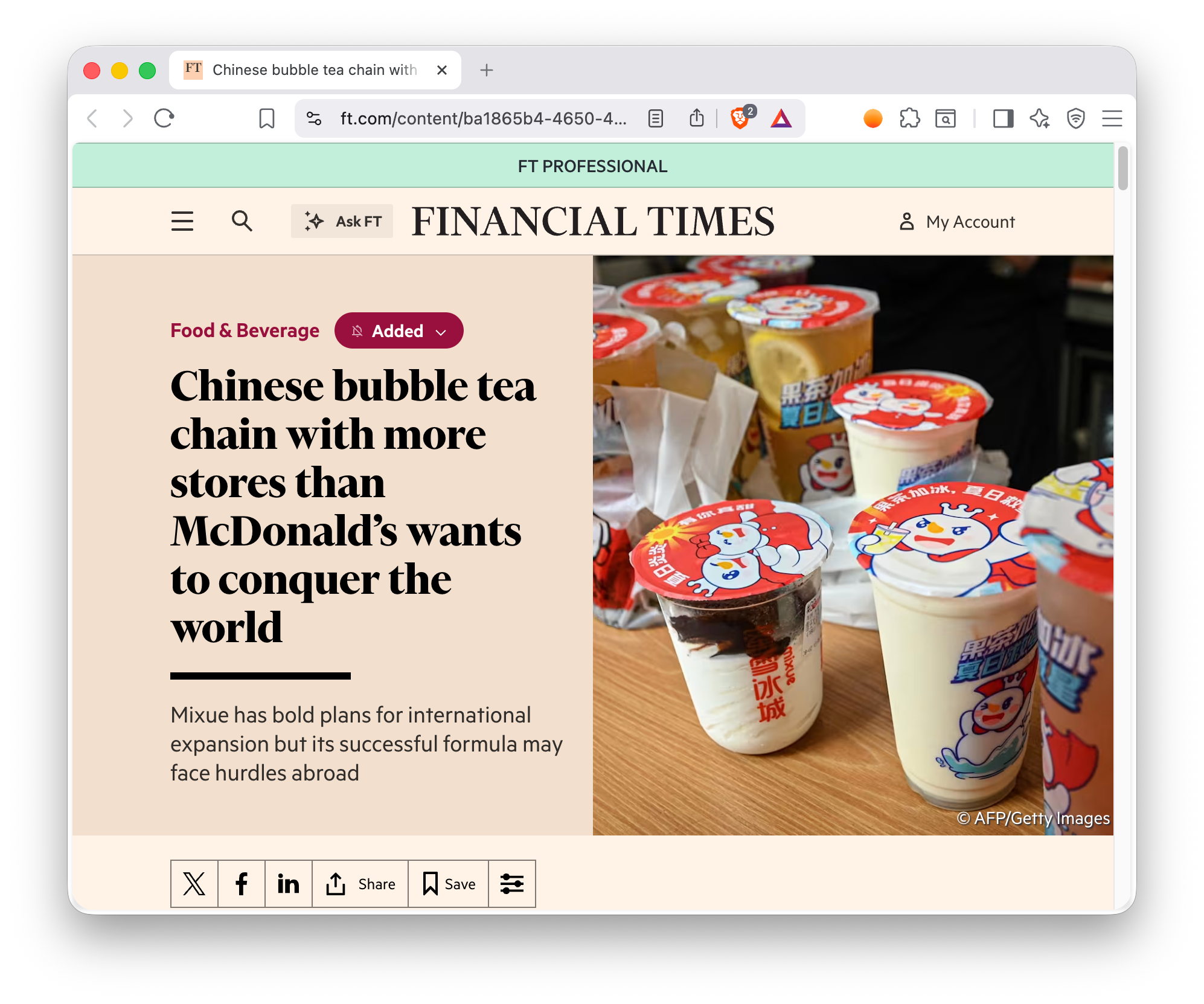

The globalization of cheap sugar

Mixue looks like a beverage chain, but strategically it behaves more like a vertically integrated logistics company disguised as ice cream. More than 60,000 stores globally, most ingredients self-produced, 29 warehouses in China, regional logistics hubs in Southeast Asia, ambitions for factories in Brazil, etc. The reason it works is simple: in a slowing economy, affordability scales better than aspiration. Starbucks sells status, and people love it, but I’d say that Mixue sells a cold dopamine hit for $1 or €1, and increasingly, global consumers seem perfectly happy with that trade.

China is beginning to export not only products, but operating systems for low-cost consumer businesses. Mixue, Luckin, Temu, Shein, these are the common denominators with ruthless supply-chain optimization combined with aggressive pricing and franchise-like expansion economics. The challenge internationally is whether the company can preserve that efficiency outside China, because the farther away it moves from its integrated manufacturing base, the more fragile the model becomes. But if it succeeds, Western consumer brands may discover that their real competitor is not another premium brand, but Chinese industrial efficiency wrapped in a cartoon snowman. FT

Google’s Fitbit Air is not really a smartwatch competitor.

At $100, screenless, cross-platform, and paired with a $10/month health coach, the point is not to give users another device to look at, but to make biometric tracking invisible and recurring. That is dangerous for WHOOP and its differentiation with "no screen, serious health data, subscription model", and Google is now offering a cheaper, more accessible version with far broader distribution.

For Apple Watch, the threat is subtler. Apple still owns the premium wrist computer category, but Fitbit Air attacks the opposite "job-to-be-done" (= less distraction, lower price, longer battery, and health coaching rather than notifications).

The broader implication is that wearables are splitting into two markets:

1/ devices that extend the phone, and

2/ devices that quietly collect health data for AI interpretation.

Apple dominates the first. Google is trying to rebuild Fitbit around the second. Bloomberg

The magic of “boring businesses”: pet shops

There is a funny thing about “boring” businesses.

They usually become interesting exactly when people stop treating the customer as rational.

If 71% of Romanian households have a pet, then this is not a niche, it is a consumer category with emotional pricing power and this is th exact point when people start buying premium food, grooming, medicine, accessories, insurance, daycare, boarding and oncology for “an animal”.

We buy it for a family member who happens to shed hair on our sofa and as pets live longer, they acquire the same wonderful economic feature as humans:

1/ recurring needs

2/ age-related problems (ie. cancer, diabetes, blood pressure, etc)

3/ higher medical complexity and owners who feel guilty saying no.

Indeed, this is a boring business.

Which is another way of saying ... "high frequency, emotional demand, fragmented services, expanding basket size, and probably better margins than many 'exciting' businesses that lose money delivering sandwiches".

Amazon Supply Chain Services (ASCS) is the AWS playbook applied to atoms.

First you build internal infrastructure at an absurd scale, after that, make it reliable because your own business depends on it, then sell the excess capability to everyone else. Freight, fulfillment, distribution, parcel delivery - this is Amazon turning its operating system for commerce into a platform for the physical economy.

The early customers matter too (e.g., P&G, 3M, Lands’ End, American Eagle). This is Amazon saying "we don’t only want to help merchants sell on Amazon. We want to run the logistics layer underneath commerce itself."

The implication is brutal for traditional logistics providers. Amazon is competing on integration, visibility, inventory positioning, forecasting, and speed. Once a company plugs into that network, Amazon learns demand patterns, inventory flows, and delivery economics across the broader economy. That is the real moat, with logistics data plus operational density.

AWS monetizes idle server capacity, while ASCS monetizes idle supply-chain capacity. The cloud was computing as a utility, but this is logistics as a utility.

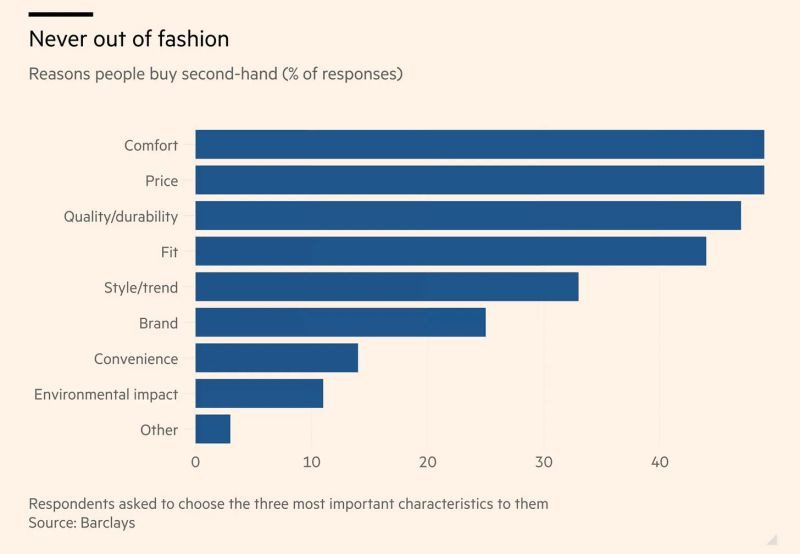

Vinted or why people buy second-hand

Vinted is what happens when a good user story meets a difficult business model. Yes, it’s worth EUR 8 bn and growing fast, but the financials tell a more complicated story. Revenue up 38%, profit down 20%, and still trading at something like 100x forward earnings if you extrapolate current growth. The reason is simple. Peer-to-peer marketplaces scale cheaply on supply, but expensively on demand. You don’t warehouse inventory, but you do spend heavily to acquire both buyers and sellers and, more importantly, to build trust in a market where quality is uncertain by default.

The deeper point is that second-hand fashion works brilliantly for consumers and awkwardly for investors. The demand side is real, driven by price sensitivity and macro pressure, not just sustainability, but the supply side is fragmented and the take rate is structurally limited. Platforms like Vinted are caught in a classic marketplace trap: lots of activity, thin margins, and constant competition from both incumbents (eBay, retailers) and new entrants.

In other words, turning “preloved” into a scalable, high-margin business is much harder than turning it into a popular one. FT

on Google (Alphabet) & Berkshire Hathaway Q1 earnings

In my latest Where is my MOAT? market update, I argue that Google and Berkshire are really two very different versions of the same posture: be patient, but for different reasons.

Google’s quarter says the AI capex is starting to work. Cloud is compounding, TPUs are becoming strategic, and part of the profit surge was really the market marking up Google’s Anthropic stake, which is another way of saying that Google is now monetizing both the AI boom and the picks-and-shovels behind it.

Berkshire, meanwhile, is doing the opposite of excitement, which is, sitting on an almost absurd cash pile, waiting for a world still too liquid and too crowded to offer Buffett-style bargains.

One company is deploying capital at an industrial scale for the future, while the other is waiting for the future to panic and come to it. WIMM

This week on “Where is my MOAT?”

6 May: [Essay] Feedback from my visit in the US

7 May: [Market update] Amazon and Apple

8 May: Q&A WIMM (on Zoom), from 17:00 (EEST, Bucharest time zone). Usually for Western Europe, that is 16:00.

10 May: [Market update] Google and Berkshire Hathaway

11 May: [Deep dive] Coca Cola

Consider subscribing to get that👇🏻 (one month free)

Thank you for being an onStrategy reader!

Interesting newsletters 💡

Endi Ungureanu - Tura de duminica