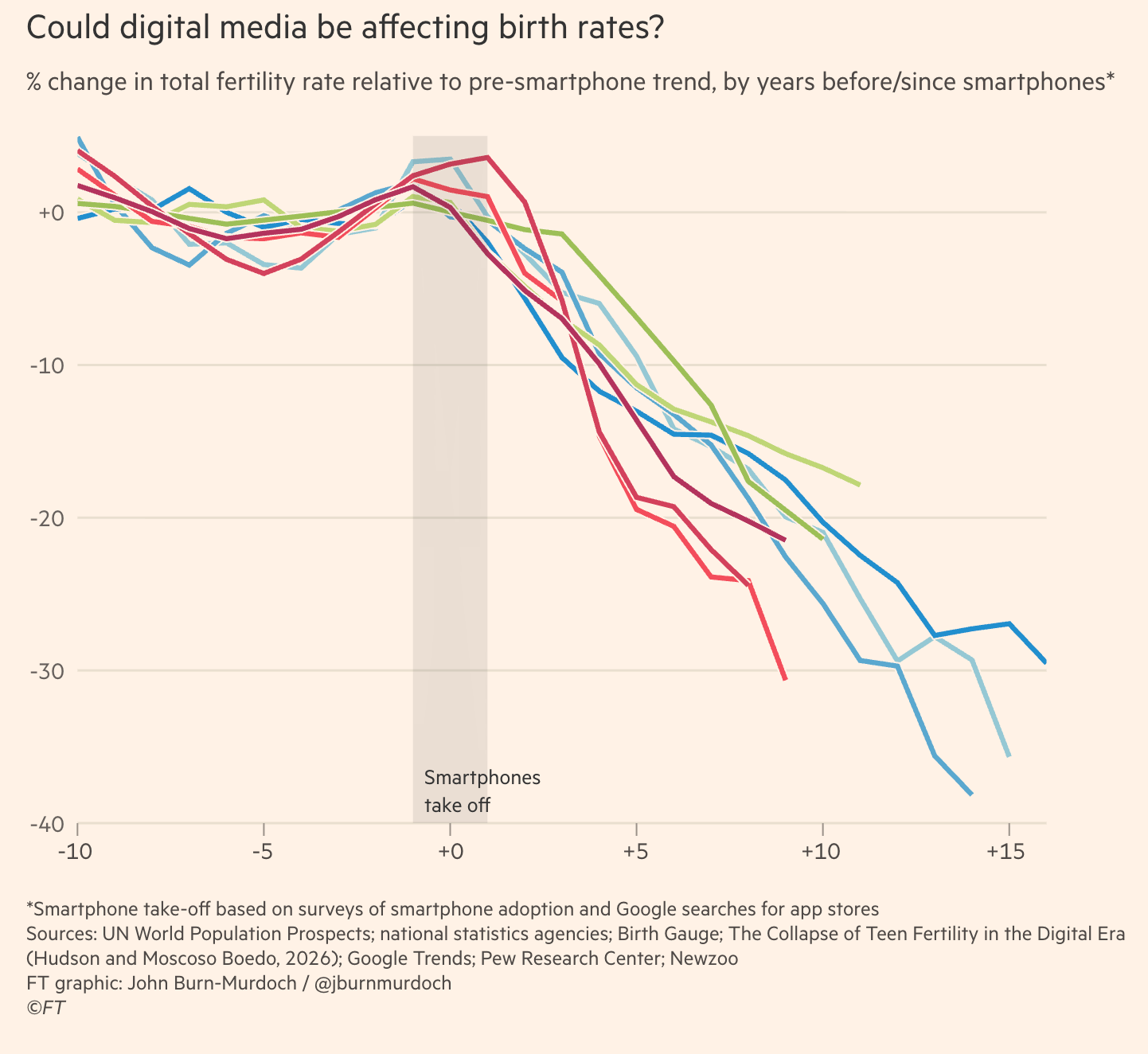

(#178) Birth decline & smartphones go hand in hand

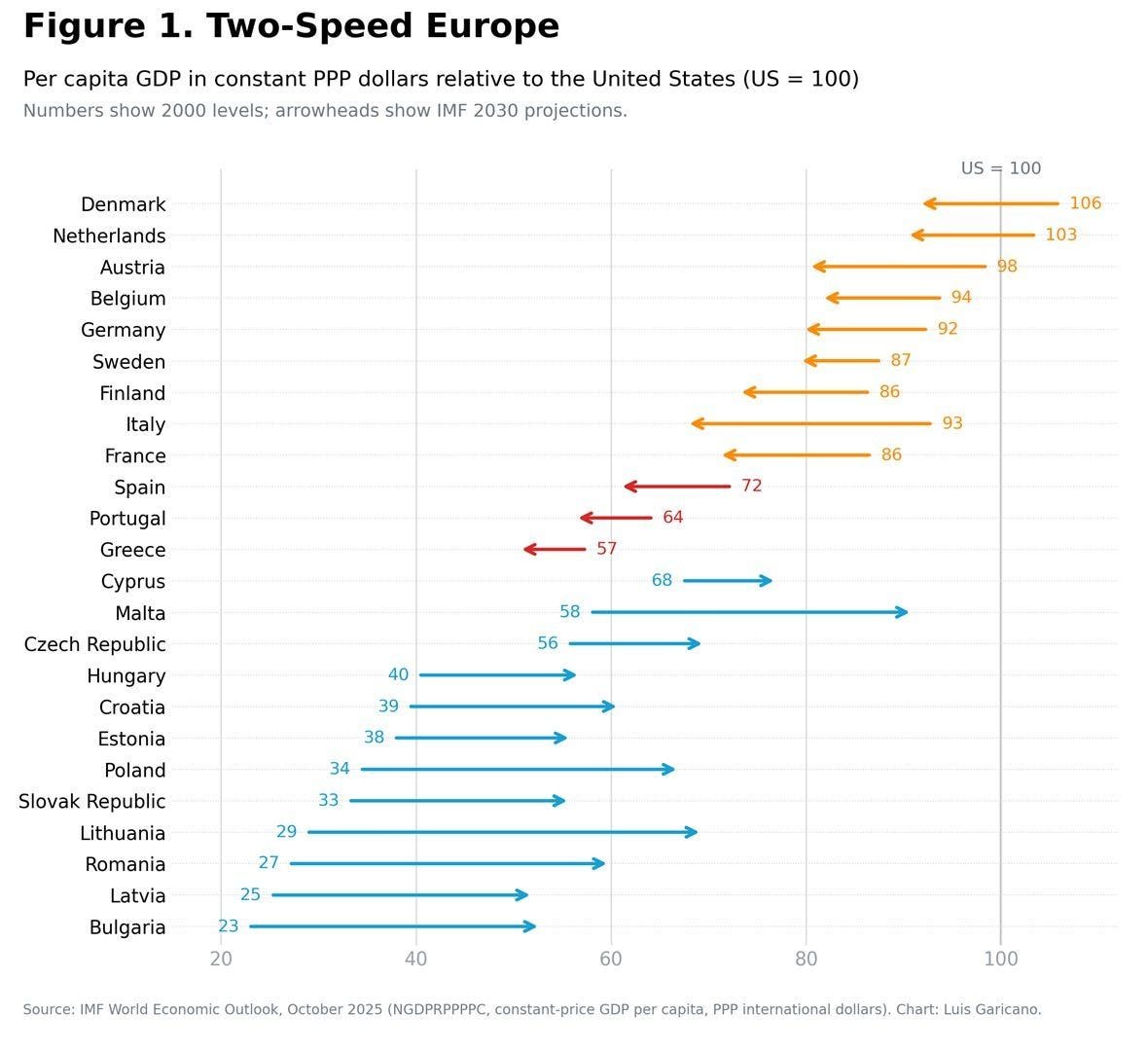

The two Europes

Dear OnStrategy Reader,

Here is what you will find in this issue:

Yes, it’s the phones!

The status of AI job automations in 2025

The two Europes

On the fertility front …in China

Meta’s Interface, Palantir Technologies’s Integration

Onto the update:

Yes, it’s the phones!

The phone is not really a phone, in the same way that a casino is not really a building with carpets. It is an attention market, a dating market, a status market, a pornography market, a beauty-standard market, a politics market, and a 24/7 comparison machine that you hand to a 12-year-old and then act surprised when, at 23, they think ordinary life is a bad deal. The polite version of the fertility story is an economic one, of course, where it shows that houses are expensive, childcare is expensive, wages are uncertain. True, but not sufficient. The sharper version is that the phone has changed the demand side of adulthood itself.

There is no smoking gun, but there is a lot of smoke. Births fell first and fastest in places that got high-speed mobile internet first. Different economies, different religions, different cultures, and different exposure to the financial crisis have the same pattern after smartphone adoption. That is not proof, but it is the kind of coincidence that eventually stops looking like a coincidence.

The mechanism is not mysterious. Fewer people meet in real life, fewer people form couples, fewer couples have children. Young people are not flirting, failing, adjusting expectations, building boring intimacy and learning how real partners actually work. They are scrolling. And scrolling is not neutral time. It is time plus ideology. It tells young women that men are disappointing, young men that women are impossible, and everyone that ordinary partners are underpriced garbage. The result is a relationship market with terrible liquidity where everyone is browsing, nobody is settling, and the bid-ask spread is absurd.

So when people say “just limit phones to one hour”, that sounds reasonable, like saying “just let the casino operate between 5 and 6 p.m”. The cost is not only the 4 or 5 hours lost every day. The cost is that the phone trains preferences in relation to what beauty means, what a partner should be, what freedom means, what compromise costs, what a normal life should look like.

Maybe the unpopular answer is the actual answer: no smartphone for children until adulthood, or as close to that as society can enforce. Not because it is elegant, liberal, or easy. Because the device is not just stealing childhood attention. It is rewriting adulthood demand. FT

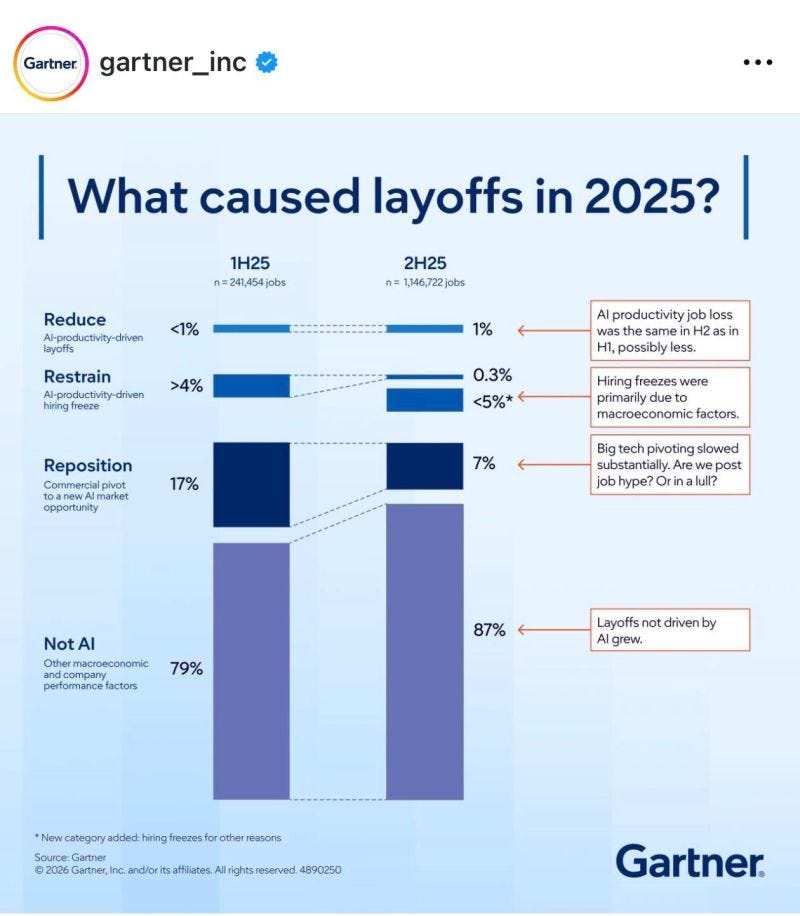

The status of AI job automations in 2025

This chart from Gartner is trying very hard to calm everyone down by saying "most layoffs were not caused by AI", which is technically true in the same way that saying "the asteroid did not directly kill the dinosaurs; the climate change afterward did".

The interesting number is not the tiny percentage of direct AI-productivity layoffs, but the “reposition” category (ie. companies restructuring themselves around AI opportunities). Because AI is not really a tool like Excel or Slack (ie. tool). It increasingly does actual work. That means firms are reorganizing around a new production function where software is no longer assisting labor but beginning to substitute for pieces of it. The market hears “AI layoffs” and imagines robots firing accountants, but the reality is more subtle. Management freezes hiring, redesigns workflows, shifts budgets, and quietly discovers that five people plus AI can suddenly do the work of eight.

Hence, I think the more important hypothesis is not replacement, but expansion (❗️). Historically, technology that lowers the cost of production tends to expand the market before it destroys the labor category. The smart company will not use AI merely to cut 10% of headcount and report one nice quarter of margin improvement. The smart company will ask something like "if the same workforce suddenly becomes 30% more productive, what additional services, customer support, product development, personalization, sales outreach, or operational responsiveness can we now offer?"

AI makes labor more leveraged. The foolish manager sees AI and thinks “fewer employees". The ambitious manager sees AI and thinks "same employees, dramatically larger company".

That is why I suspect the long-term winners will not be the firms that replace people fastest, but the firms that combine people and AI into a much more scalable organization.

The two Europes

Europe looks like 2 companies sharing one ticker: Eastern Europe is the growth subsidiary, while Western and Southern Europe is the legacy conglomerate explaining that, yes, productivity is weak, energy is expensive, defense is underbuilt and startups do not scale, but the compliance department is having a fantastic decade.

The East is converging because EU accession, investment, lower legacy welfare burdens and fear of Russia create urgency. The West is drifting because France, Italy, Spain, Portugal and Greece have built beautiful museums of social protection around economies that increasingly cannot pay for them.

Mario Draghi says Europe needs innovation, energy, defense and scale, but Brussels says something like "excellent, please first complete Form 19-B on sustainable stapler procurement".

Europe has a growth story.... just mostly in the part Europe used to lecture. LINK

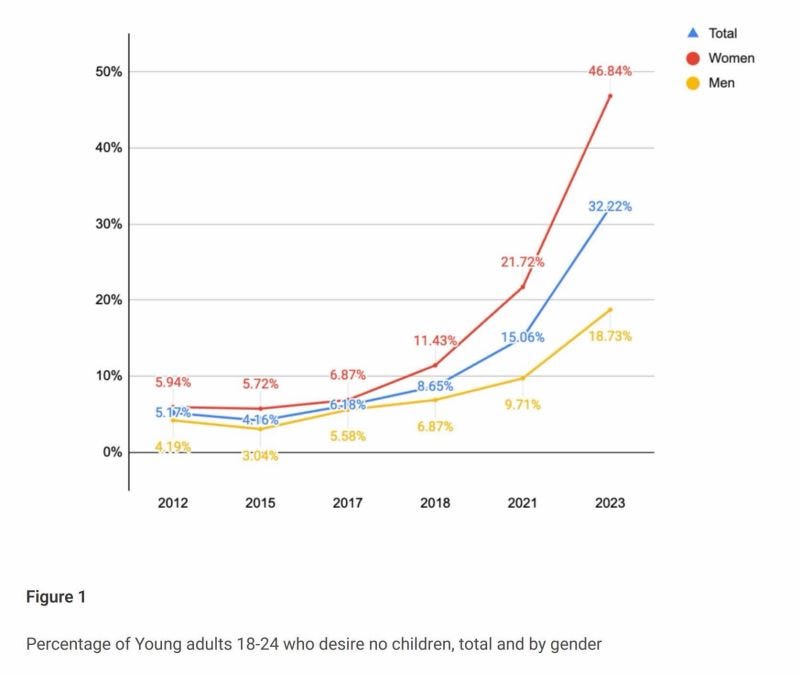

On the fertility front …in China

In 2012, zero fertility desire among 18–24-year-olds was a niche view, around 5%; by 2023 it was 32%, and among young women almost 47%.

The old East Asian fertility model was baded o the asumption that people still want children, but housing, education, work hours, marriage markets, and family norms make the trade impossible. This paper suggests something more dangerous. Constraints are becoming identity.

Young women are not merely saying “I cannot afford the second child”. Many are saying “I do not want the first contract“ and that matters because China’s policy machine is built to solve supply problems (build apartments, subsidize nurseries, adjust hukou, issue slogans), but this is a demand problem.

Parenthood is being evaluated like a bad investment with high upfront cost, lifelong lock-up, unequal labor allocation, weak partner governance, career dilution, and social pressure masquerading as shareholder value.

Beijing spent decades teaching households that children were a state-managed variable. Now educated young women have learned the lesson too well and are managing the variable themselves. The state wants demographic growth, but the consumer wants optionality, and in modern societies, optionality usually wins. LINK

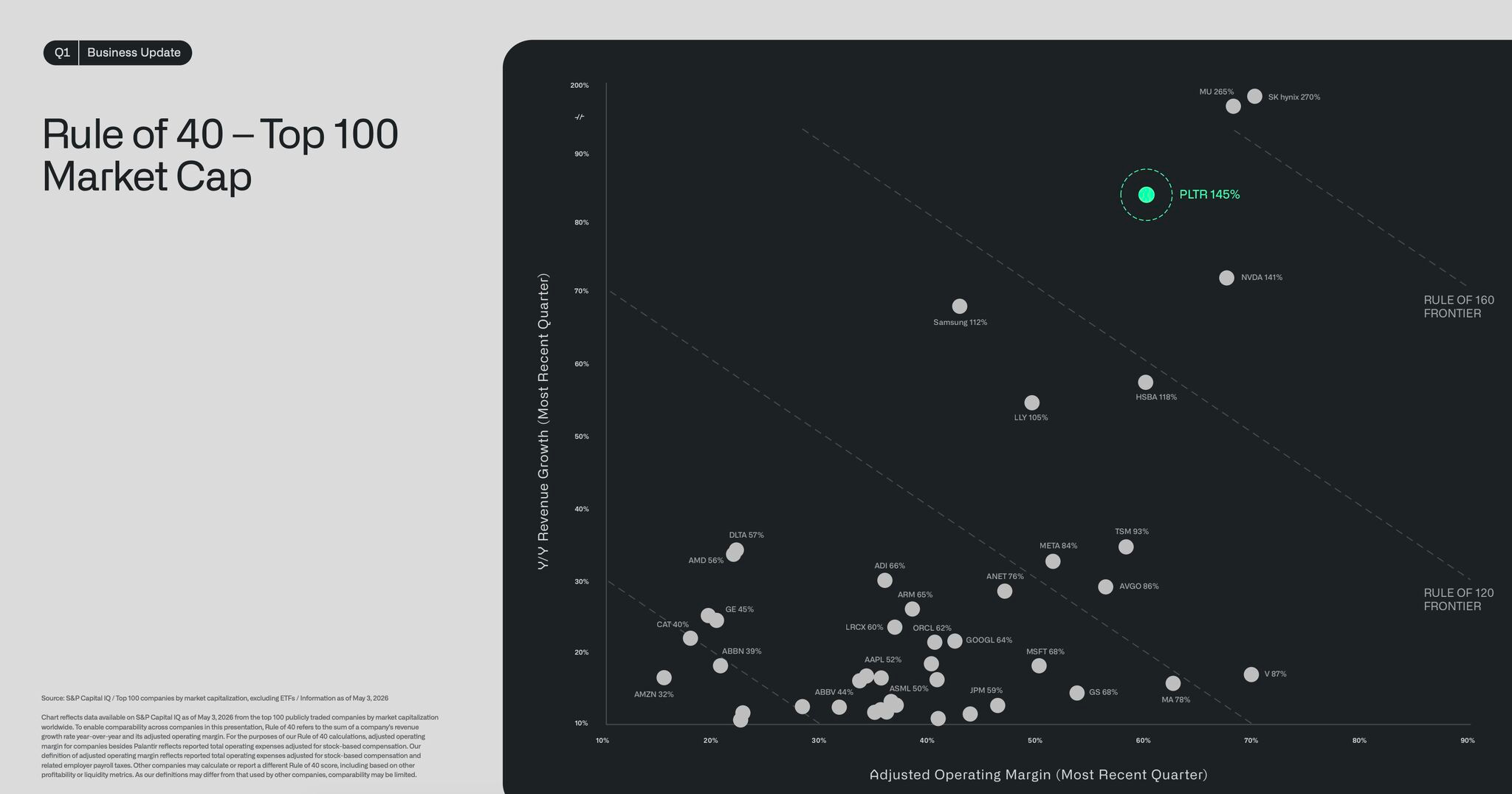

Meta's Interface, Palantir Technologies's Integration

In my latest Where is my MOAT?, I look at Meta and Palantir, two companies trying to prove very different AI stories.

The bigger story is that Meta may have one of the clearest consumer AI opportunities in the market, with billions of users, daily habits, social graphs, creators, commerce, identity, and eventually glasses.

Palantir is the opposite case. The company is excellent, the Rule of 40 numbers are stellar, and Alex Karp’s ambition remains unmatched. But valuation matters. At a very high multiple, Palantir must prove that enterprise AI belongs to its ontology and operating system, not to cheaper, easier, more intuitive tools from Anthropic, OpenAI, or Databricks. WIMM

This week on “Where is my MOAT?”

13 May: [Watchlist] The expected IPO of Cerebras

14 May: Portfolio update

15 May: Macroeconomics (May 2026)

16 May: [Market update] META and Palantir

17 May: [Deep dive] JPMorgan

Consider subscribing to get that👇🏻 (one month free)

Thank you for being an onStrategy reader!

Interesting newsletters 💡

Endi Ungureanu - Tura de duminica