(#180) GoPro is dead, and they know it

Case study: Amazon - AI usage is not AI value

Dear OnStrategy Reader,

Here is what you will find in this issue:

GoPro is dead, and they know it

Case study: Amazon - AI usage is not AI value

Robinhood’s agentic can trade 24/7…for your

Europe and (bad) demographics

on Ferrari Luce 🚗

Search becomes the answer layer

On to the update:

GoPro is dead, and they know it

GoPro is another reminder that inventing a category is not the same thing as controlling it. The company gave the world the action camera, built the brand, owned the lifestyle, and turned “GoPro” into a verb. But the center of gravity in consumer hardware has moved from brand storytelling to supply-chain velocity. DJI and Insta360 (both Chinese) are both faster product organizations sitting closer to the manufacturing ecosystem that now defines the category. After years of funding and innovation, they now have bigger sensors, better stabilization, stronger thermal management, more features, faster iteration. They are the compounding returns of being embedded in the hardware stack. Nikkei reports that the company is now exploring a potential sale after years of declining revenue, while DJI and Insta360 gain ground with higher-performing products.

The implication is uncomfortable for the West. Hardware is not won by “having a great brand” plus outsourcing the hard parts. It is won by dense supplier networks, manufacturing feedback loops, component access, engineering talent, and the ability to launch, learn, and relaunch faster than the incumbent can hold a board meeting. China’s advantage here is system speed. A company like DJI can learn from drones, cameras, sensors, batteries, gimbals, thermal systems, software, and creators, and only then redeploy that learning across adjacent categories.

This is where government subsidies matter, but not in the simplistic “give money to a national champion” sense. The United States and Europe often subsidize factories after the market has already moved. China subsidized entire ecosystems for suppliers, industrial parks, export capacity, engineering density, battery chains, electronics assembly, and patient iteration. That matters because consumer hardware is a supply-chain sport. A subsidy that produces one plant is useful, but a subsidy that produces a cluster is strategic. The lesson from GoPro is that industrial policy should not ask, “Can we save this brand?” It should ask, “Can we rebuild the capability base that lets the next GoPro scale before the next DJI arrives?”

GoPro’s possible sale is an industrial policy story. America still creates categories (eg. action cameras, smartphones, social media, AI models, creator platforms), but China increasingly industrializes them at speed. The question for Western governments is whether they want to subsidize demand, protect incumbents, or rebuild supply. Only the third option changes the outcome. Because in hardware, the moat is the chain of companies behind it. LINK

AI usage is not AI value

Amazon has discovered a basic law of corporate metrics, which is that when you give employees a leaderboard, they will optimize for the leaderboard. This is charming when the metric is sales, slightly weird when the metric is meetings, and expensive when the metric is AI tokens consumed. The company reportedly shut down an internal "Kirorank" leaderboard after employees used AI agents to generate extra activity and climb the rankings, which is a very modern situation where the humans instructed the robots to create useless work so the humans could appear more committed to the robot future 🫠. This is adoption theatre with a GPU bill attached.

The real question is output. Using AI 5 times, 500 times, or 5 million tokens worth of times matters only if something valuable comes out, like better code, faster deployments, fewer bugs, improved products, lower costs, happier customers. Maybe the spending is justified. Amazon expects enormous AI capex, and a company at that scale can rationally burn compute if it produces better internal tools, stronger developer velocity, or defensible product improvements. But the unit of analysis has to move from "how much AI did you use?" to "What did you build, what changed in the business, and what cash flow does it touch?". Which is why Amazon’s shift toward measuring "normalised deployments" and useful code makes sense.

In capitalism, tokens are an input, but products are the output. Everything else is a very expensive scoreboard. FT

Robinhood’s agentic can trade 24/7…for your

Robinhood’s agentic trading story is about the next abstraction layer in retail speculation. Agentic trading turns a sentence into a strategy with commands like “rebalance my portfolio”, “build me an AI basket”, “buy oversold stocks”, “monitor semiconductors”, and “later trade options, crypto, futures, and event contracts”. The product becomes execution itself where the user intent goes in, trades come out.

The economic model is straightforward. Zero-commission trading makes high-frequency small-account strategies feel free to the user, while the market structure still monetizes activity through spreads, routing, and market-making economics. For Robinhood, agentic trading expands the surface area of order flow. More automation means more engagement, more transactions, more data, and more opportunities to convert attention into financial activity.

The strategic risk is convergence. Personalized AI strategies may turn into the same 20 retail instincts running at machine speed, which are focused on buying the dip, chasing momentum, rotating into AI, selling volatility, gambling on options, and so on. That creates predictable flows, and predictable flows create alpha for whoever trades against them. Robinhood is becoming a consumer financial operating system, where investing, credit cards, sneakers, restaurants, and prediction markets all become conditional spending, summarized by “when X happens, allocate my money”. LINK

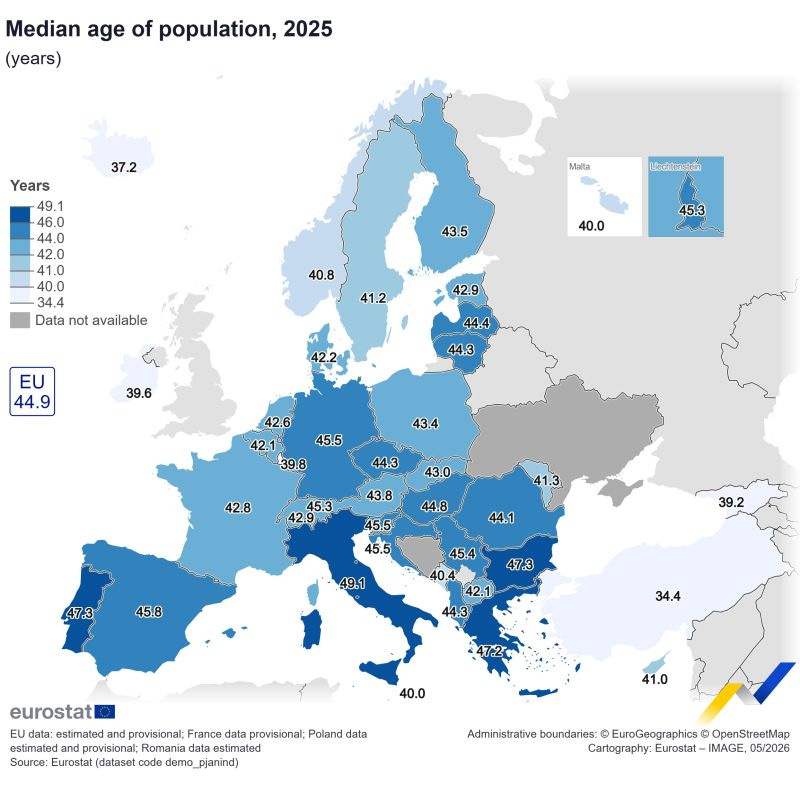

Europe and (bad) demographics

🇪🇺 Europe’s median-age map is a useful reminder that demography is the operating system. A country with a median age of 49 is not simply "older" than one with a median age of 34. It has a different discount rate. Older societies vote differently, consume differently, invest differently, and regulate differently. They place a higher premium on stability, predictability, healthcare access, asset protection, and low volatility. That makes sense individually, but it compounds into a macro problem where the institutions most capable of protecting accumulated wealth are not always the institutions most capable of creating new wealth.

This is why Europe’s demographic challenge is less about population decline in the abstract and more about capital allocation. Aging societies tend to shift resources from formation to maintenance, from housing construction to housing preservation, from education to pensions, from risk capital to safe assets, from migration to identity politics, from productivity experiments to compliance systems. That is fine if the asset base is exceptional, and Europe’s is the home of many brands, infrastructure, industrial depth, universities, tourism, dense cities, and social trust. But it means Europe increasingly looks like a high-quality legacy business with declining organic volume growth.

The optimistic interpretation is that Europe can become a premium, automation-heavy, scarcity-based economy. Fewer workers can still support more output if capital deepening, robotics, AI, energy productivity, and high-value services scale fast enough. In that model, 🇮🇹 Italy is not "too old", but a portfolio of luxury, tourism, design, precision manufacturing, food, and patrimony monetized globally. 🇩🇪 Germany is not just demographically challenged, but an industrial balance sheet that must swap cheap energy and export volume for automation and software leverage. 🇷🇴 Romania, at 44.1, is not young, but it still has some demographic room relative to Southern Europe , if it can convert labor, education, and migration flows into productivity before aging catches up.

The pessimistic interpretation is that Europe becomes a continent of beautiful fixed assets and rising transfer claims. The danger is that the political economy becomes optimized for preserving yesterday’s promises with tomorrow’s shrinking workforce. That produces the familiar European equilibrium with high savings, low risk appetite, expensive housing, slow permitting, underbuilt infrastructure, cautious incumbents, and young people asked to be entrepreneurial while paying for a system designed before they were born.

The real question is not “Is Europe old?" because the map answers that. The question is whether Europe can raise productivity faster than it raises dependency ratios. It needs a model where fewer people can produce much more, otherwise the continent becomes a very elegant annuity with a growth problem, and zero growth is a "zero-sum" game. LINK

on Ferrari Luce 🚗

Everyone can make a fast EV now because acceleration has been commoditized by batteries in the same way that high-frequency trading commoditized being quick.

Ferrari’s problem is whether it can make silence feel expensive. Combustion engines gave Ferrari a free emotional dividend with noise, vibration, danger, and theater. Electric motors give you torque and efficiency, which are nice, but also vaguely appliance-like. That's why Ferrari has spent 5 years and 40,000 kilometers developing an acoustic character that captures and amplifies the hum of the electric motors, because apparently, the future of Italian passion is a sensor on the rear axle.

Still, this may work, because Ferrari’s real moat was never just the engine, but the allocation, ritual, waiting lists, resale mythology, and the ability to convince rich people that buying the impractical thing is rational because too few other people are allowed to buy it. Therefore, the Luce is a scarcity test with batteries, and not an EV test. Bloomberg

Search becomes the answer layer

🔎 In my latest Where is my MOAT? investor brief, I ask a simple question: "Is Google still defending search, or is search quietly becoming something else?"

The old search business monetized intent, where you typed a query adn Google sold the click. The new search business monetizes the answer, the follow-up, and eventually the action. That is a very different game.

Classical search is still enormous. Google Search & Other generated $224.5B in FY2025, while the global search advertising market is around $268B in 2026. But the surface is changing fast because ChatGPT runs 2.5B prompts per day, AI Overviews now appear in a meaningful share of Google searches, and answer engines reduce blue-link clicks while increasing the value of the session.

That is why the next 5 years are not about "Google dies" or "ChatGPT wins". They are about who owns the answer layer on top of the query layer.

🤔 So, who captures the next search market: the company that owns the query, or the company that owns the answer? WIMM

27 May: Apple, the Band, and the 2016 Decision that compounds

29 May: Search + Generative Search: TAM, shift, and who captures It

30 May: Ferrari’s Electric Test

31 May: [Deep Dive] IBM

Consider subscribing to get that👇🏻 (one month free)

Thank you for being an onStrategy reader!

Interesting newsletters 💡

Endi Ungureanu - Tura de duminica

The same outperforming of western competitions through vertical integration can be seen in the automotive industry also. And it's very interesting to see how the Chinese are creating competitive edge in AI, not through being best but by having the lowest inference cost.

China and the west are competing through very different operating models, and it doesn't look good for the west.