(#161) Sony, TCL, and the Unbundling of Hardware and Brand

Have we reached the peak of Social Media?

Dear onStrategy Reader,

You can now start a one-month free trial for “Where is my moat?”

You won’t get my portfolio structure during the trial period, but you’ll get enough information and insights that can convince you if it’s worth it or not.

👉 Give it a try:

💬 Thoughts on Discord’s IPO implications and trade-offs

Discord’s IPO is a little bit like taking your favorite dive bar and putting it on the Nasdaq. For years, Discord has thrived in a cultural niche because it was (is) part Slack, part Reddit, part secret clubhouse where Gen Z can talk memes, games, mental health, AI image prompts, and homework… often all in the same thread. With 200 million monthly active users and $600 million in revenue, it’s a real business now, not just a gamer side hustle. But now comes the hard part: telling the Wall Street story without killing the vibe. Discord makes money from subscriptions (Nitro) and some experimental ad products, but it’s not clear whether its charming chaos can coexist with the demands of quarterly earnings calls and EBITDA margin targets.

The problem is that Discord was never designed to scale like a traditional tech platform. On the contrary, it was optimized for intimacy, not monetization. Communities are siloed, content isn’t algorithmically pushed, and users are fiercely allergic to being treated like monetizable eyeballs. That makes it hard to inject ad dollars at scale without breaking what makes Discord feel authentic. Authenticity doesn’t pay the bills or justify a unicorn valuation. The new CEO, who helped sell Activision to Microsoft, probably knows this. But selling games and selling ads are two very different businesses, and it’s unclear whether Discord wants to become more like Reddit (content ad tech) or Zoom (enterprise SaaS). Either path requires trade-offs that risk alienating users or disappointing investors… or both.

Also, let’s not forget the real risk. This is a social platform with lawsuits, regulatory attention, and a long history of being a safe haven for chaos, extremism, and under-moderated content. That’s not the kind of thing that underwriters love to highlight in roadshows. But if the IPO does go ahead and if Discord manages to monetize without over-monetizing, it could become a case study in how to take a messy, beloved corner of the internet and give it a market cap without killing the culture. Or it could become the next cautionary tale in the long list of social platforms that tried to grow up and lost their soul in the process. Either way, the IPO deck better be really, really good. Bloomberg

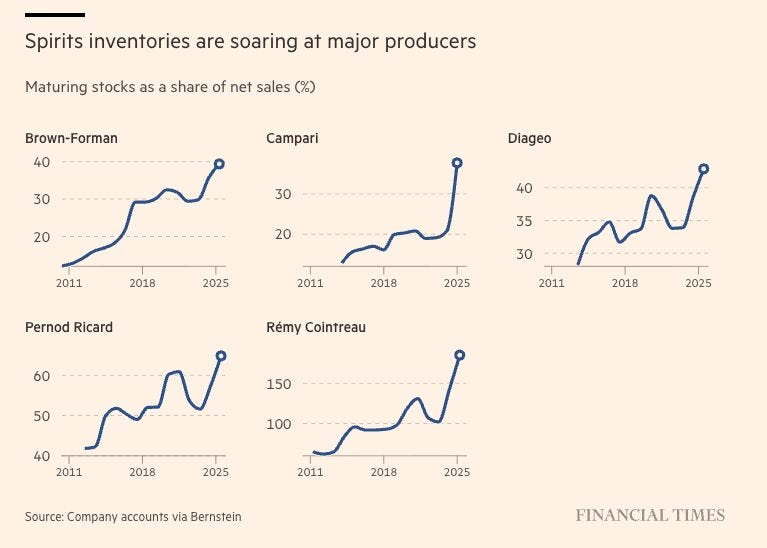

on (drinking) alcohol 🥃

Imagine borrowing money at near-zero rates to distill the finest Cognac, then aging it for half a decade while your customer base suddenly discovers sobriety (hey, Gen Z), semaglutide, and... sparkling water 😅

That’s where we are. The world’s biggest booze brands (Diageo, Pernod Ricard, Campari, Brown-Forman, and Rémy Cointreau) are sitting on $22 billion worth of aging spirits that nobody wants. Inventory-to-sales ratios are through the distillery roof. Remy’s stockpile alone is 2x its annual revenue and nearly equals its market cap. They bet big on COVID-induced drinking being a forever trend. It wasn’t.

The hangover hit these producers, but not just from the macro squeeze on discretionary spend, but also from the rise of health culture and drugs that literally make you not want to eat or drink.

Current status: Jim Beam’s main distillery is shuttered, Diageo has halted whiskey ops in Texas and Tennessee. Also, they can’t cut prices too much because… debt. When you’ve levered up to fund barrels that take 10 years to mature, fire sales become balance-sheet disasters.

What a strange place to be. Caught between a whiskey lake and a dry consumer, which one might come up with something like “drunk on CapEx, sobered by demand”.

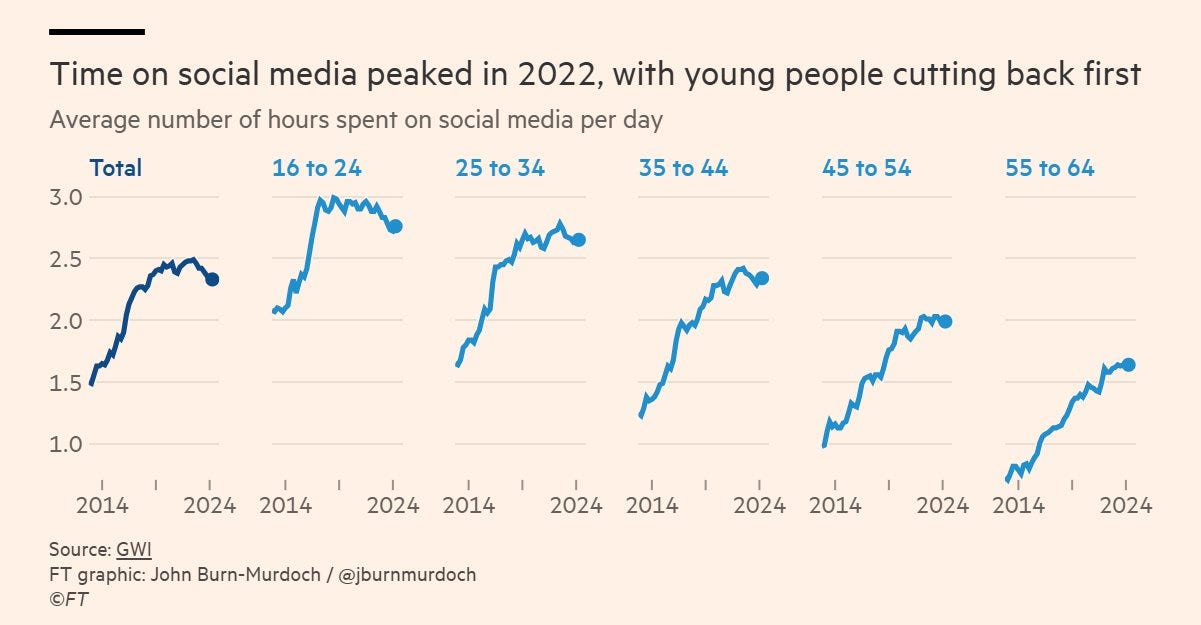

The peak of Social Media?

There’s a kind of poetic justice in the idea that Gen Z, the very cohort that made TikTok dance trends and Instagram filters part of the cultural oxygen, is also the first to start cutting back on social media use. The FT chart makes it clear. Time spent on social platforms peaked around 2022, and it’s the youngest users who are leading the retreat. Maybe it’s digital fatigue, or maybe it’s just that the dopamine loops are less satisfying when everyone’s chasing the same algorithmic clout.

Either way, it’s bad news for engagement-driven ad models, especially those banking on infinite scroll as their economic engine, and probably good news for, I don’t know, walking outside?

The under-35 crowd has always been the canary in the monetization coal mine, and if their screen time is dropping, it means ad inventory is flattening, user growth is maturing, and the attention pie isn’t growing the way Meta and Snap were hoping.

Sure, older users are still ramping up, but you can only grow MAUs so long on the backs of 55-year-olds discovering Facebook Marketplace. Social media will not die, but the era of effortless exponential growth might be, and for companies built on selling engagement to advertisers, or VCs, this looks a lot like the beginning of a post-peak internet attention economy.

End of an era: TLC (China) buys Sony’s home entertainment business (Japan)

Sony sold its soul for margin. Or at least 51% of its Bravia TV business, which is pretty close. In a move that feels less like strategy and more like surrender, Sony is handing over control of its home entertainment unit to China’s TCL…. the budget-TV behemoth that’s now taking over the big boys’ toys. This new joint venture means TCL will manufacture TVs branded “Sony” and “Bravia”, but using TCL’s display tech. Which is a little like buying a Rolex and finding out the engine is from Casio. Sony gets out of a low-margin business, TCL gets brand credibility, and investors get…confused nostalgia.

Of course, it makes perfect sense. Bravia, for all its glossy ads and cinematic purity promises, was never really about TVs. It was a relic of the old Sony, the one that thought hardware margins could still pay for Tokyo real estate. These days, Sony is more Netflix than Panasonic. It wants you to buy anime subscriptions and Spider-Man tickets, not quibble over contrast ratios at Best Buy. Of course TCL is happy to build everything for everyone, so long as they can slap on someone else’s logo and sell you the remote. It’s outsourcing with a licensing twist or IP as the moat, margin as the master.

Who can blame them? Sony’s operating profit margin on TVs is a rounding error, while its media and gaming assets are IP gold mines. TCL gets distribution, Sony gets to look focused, and Bravia gets to live on as a ghost in the machine, whic is, beautiful on the outside, Chinese on the inside.

Just don’t be surprised when your Sony TV starts recommending Chinese products and services by default. Or, in a few years, when Sony sells the other 49% and says it was never in the TV business to begin with. Bloomberg

Thanks for reading onStrategy! Subscribe for free to receive new posts and support my work.

WIMM - Where is my MOAT?

If you enjoy my strategy notes on LinkedIn or in OnStrategy, WhereIsMyMoat.com is the deeper, “skin-in-the-game” version: full theses, moat scoring, and a clear view of the company’s future performance.

Last week’s analysis:

🤓 The logic of my secondary portfolio (only for paying subscribers)

My stock picks for 2026 (only for paying subscribers)

This week’s analysis:

22nd January - Essay] 🛍️ The Next Shopping Platform is an Interface

23rd January - 📈 The Two-Broker Strategy (what investing apps are out there)

24th of January - 👟 The Great Nike Reset

25th of January - 🩴 The Comfort Economy and Birkenstock’s Moat